Supply Chain Analyst Tactics: Cut Freight, Boost Turns

Litens Aftermarket didn't hire Jack Paruszkiewicz to manage spreadsheets. They hired him because he previously boosted item turns by nearly 50% at General Fasteners. This move signals a hard pivot in our industry: the AI hype cycle has collapsed, replaced by a demand for proven operational returns. As Infor notes, 2026 strategies now focus strictly on embedding AI use cases that deliver measurable value in risk management rather than chasing theoretical promise.

This article dissects the strategic role analysts play during complex expansions, specifically Litens' integration of the Dolz water pump brand. We will examine the mechanics of inbound freight, where Paruszkiewicz utilized consolidated shipping to curb transportation spend across high-volume supplier bases. We will also dissect practical inventory reduction tactics that free up working capital without disrupting warehouse operations.

Forget generic growth forecasts. Real modern distribution requires granular execution. By applying specific cost-saving strategies, organizations can replicate efficiency gains seen in top-tier industrial sectors. Targeted supply chain optimization transforms raw data into actionable logistical dominance for aftermarket providers facing aggressive scaling.

The Strategic Role of a Supply Chain Analyst in Modern Distribution

Defining the Supply Chain Analyst Role Beyond Logistics

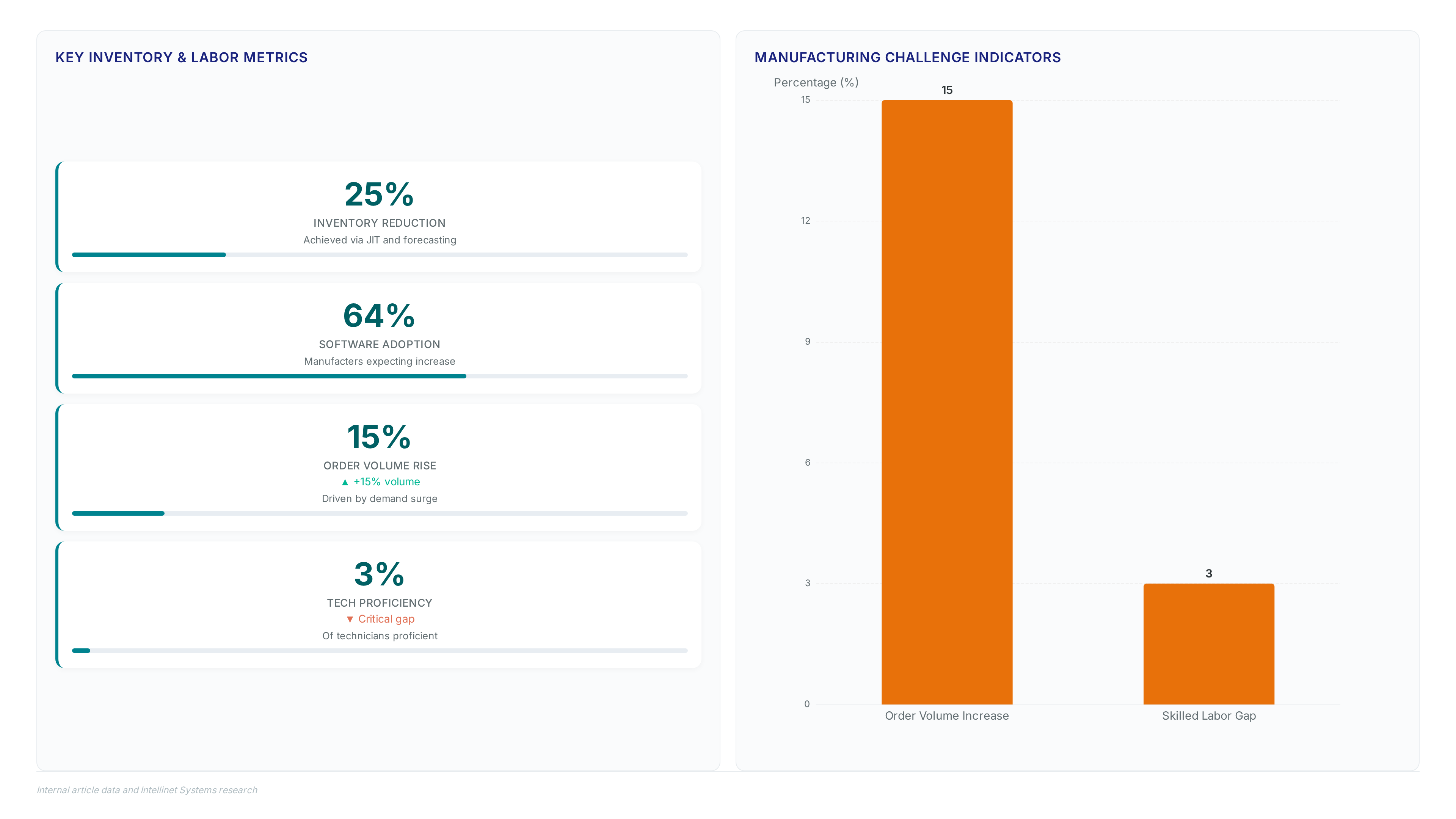

Stop treating the supply chain analyst as a logistics coordinator. This role optimizes inbound freight and inventory levels, period. Supply chain costs have risen by 15% due to order volume increases and logistical complexities, making passive observation unacceptable. The position demands navigating specific leadership hierarchies to execute cost savings effectively. At Litens Aftermarket, Jack Paruszkiewicz reports within a structure including Brad Long and Vikram Sherwal to align procurement with distribution goals. This reporting line ensures that inventory reduction projects directly support warehouse operations in Toledo. History proves that specialized oversight beats standard buying functions every time.

Mechanics of Inbound Freight Management and Warehouse Operations

Mechanics of Inbound Freight and Warehouse Support Workflows

At Litens Distribution Inc, inbound freight management converts shipment tracking into immediate warehouse support actions. Passive data entry is obsolete. The mechanism requires synchronizing arrival manifests with physical dock capacity to prevent bottlenecks during high-volume intake periods. Operators must validate carrier claims against purchase orders before goods enter the Toledo facility floor.

- Verify inbound shipment manifests against procurement records.

- Allocate dock space based on real-time inventory levels.

- Route received goods to specific storage zones for rapid retrieval.

Competitors like Dorman Products compete on distribution speed, forcing Litens Aftermarket to optimize every handoff. The supply chain analyst bridges the gap between digital tracking systems and physical handling crews. Without this coordination, expanding SKU counts from brands like Dolz create unmanageable storage congestion.

| Workflow Stage | Traditional Approach | Optimized Mechanism |

|---|---|---|

| Arrival Notification | Manual phone calls | Automated EDI alerts |

| Put-away Logic | First-available space | Velocity-based zoning |

| Inventory Update | End-of-day batch | Real-time synchronization |

Legacy infrastructure creates the bottleneck; it cannot support the real-time data exchange modern velocity demands. Failure to integrate these systems delays cost savings realization. Disjointed workflows increase dwell time and erode margin on every pallet received.

Managing Supply Chain Complexity During Dolz Brand Expansion

Integrating Dolz requires synchronizing European inbound freight with domestic SKU launches to prevent dock congestion. Acquiring this 90-year brand introduced thermal management lines demanding distinct handling protocols compared to legacy belt drive products. Operators must track inventory by validating arrival manifests against procurement records before goods enter the Toledo facility floor. This step prevents erroneous stock entries that distort visibility during high-volume intake periods. The sheer scale of recent expansions drives the challenge, such as the July 2025 launch covering over 160,000 vehicles.

Manufacturers increasingly adopt supply chain management software to mitigate risks from geopolitical tension and demand shifts. Order volume spikes drive significant cost increases due to logistical friction. Proven tracking depends on aligning physical dock space with real-time data feeds rather than static schedules.

| Integration Factor | Legacy Belt Drive | Dolz Thermal Line |

|---|---|---|

| Origin Point | Domestic/Nearshore | European Import |

| Lead Time | Short Cycle | Extended Transit |

| Storage Zone | High Velocity | Climate Controlled |

Rapid expansion breaks standard operating procedures when import volumes surge. New SKUs displace established inventory without updated workflows, causing retrieval delays. Personnel must execute a rigid sequence: verify carrier claims, allocate zone-specific storage, and update system quantities immediately. Mixing these new product lines with existing stock creates pallets that stall outbound shipping. Specialized analysts counter the disorganization inherent in merging disparate supply chains. Products and Brands must prioritize clear segregation protocols to maintain throughput velocity.

The industry expects increased adoption of management software to mitigate risks from tariffs and geopolitical tension. Yet, without strict inbound freight scheduling, software merely reports delays faster rather than preventing them. Products and Brands solutions should focus on synchronizing physical dock capacity with digital arrival windows to close this gap.

Inventory Reduction Projects and Cost-Saving Strategies in Practice

Application: Item Turns as the Primary Metric for Inventory Reduction

Item turns quantify distribution efficiency by dividing annual sales volume by average inventory, distinguishing active throughput from static stock counts. This metric isolates the success of reduction projects better than raw unit tracking because it accounts for demand velocity. Simple stock counting fails to reveal capital inefficiency until obsolescence occurs. Operators must prioritize velocity over volume to avoid margin erosion during expansion phases. Unlike static counts, turn analysis exposes slow-moving SKU bloat before it becomes a write-off liability.

Strategic alignment requires shifting focus from hype-driven technology to embedded use cases that deliver proven returns in daily processes.

Stagnant inventory turns trap working capital that operators cannot redeploy for urgent procurement needs. High-volume distributors face immediate liquidity constraints when slow-moving parts occupy warehouse space intended for fast-turn SKUs. This cost pressure compounds when capital remains locked in static stock rather than funding new inbound freight cycles. Competitors like Gates operate in the same high-volume belt drive space where economies of scale typically drive unit costs down, making excess stock even more punitive for smaller players. Reducing stock levels without demand forecasting accuracy risks stockouts on critical aftermarket components. Operators must balance lean inventory targets against the volatility of aging vehicle fleets requiring sporadic part availability. Failing to optimize this balance leaves significant recoverable capital inaccessible during expansion phases. Releasing trapped cash requires shifting focus from total unit counts to velocity metrics that reflect actual sales throughput.

Comparing Inventory Management Approaches in Aftermarket vs OEM Environments

Defining Aftermarket Volatility vs OEM Stability in Supply Chains

Aftermarket volatility stems from rapid SKU proliferation following acquisitions like Dolz, contrasting sharply with fixed OEM production lines. Original Equipment Manufacturers optimize for steady-state outputs, whereas aftermarket distributors manage erratic demand spikes across aging vehicle fleets. This structural divergence forces suppliers to adapt to AutoZone's Mega-Hub strategy, which prioritizes slow-moving part availability over pure velocity. The U. S. Light-duty sector is projected to grow 5.2% year-over-year in 2026, accelerating the need for flexible inventory buffers. Global forecasts reach $804.82 billion by 2029, yet this expansion introduces significant supply chain friction.

| Dimension | OEM Environment | Aftermarket Environment |

|---|---|---|

| Production Trigger | Fixed build schedules | Reactive replacement demand |

| SKU Stability | Low variation per model year | High variation from acquisitions |

| Inventory Risk | Obsolescence at model end | Fragmentation across 160k+ VIO |

| Lead Time | Predictable quarterly cycles | Volatile daily replenishment |

Maintaining broad coverage while avoiding capital stagnation creates immediate tension. Unlike OEMs, aftermarket firms cannot rely on linear demand models when integrating brands with 90 years of history. Misalignment results in acute cash entrapment in slow-turn assets. Successful navigation requires deploying cloud-based visibility tools to track these disjointed flows. Failure to distinguish these modes results in stockouts for critical repair parts while warehouses fill with irrelevant units. Strategic differentiation now depends on managing this inherent instability rather than suppressing it.

Applying Analyst Roles to Manage Dolz Brand SKU Proliferation

Specialized analyst roles directly mitigate the inventory bloat caused by adding 90-year-old European brands like Dolz to North American catalogs. Paruszkiewicz now applies cross-sector experience to prevent capital lock-up as the portfolio expands beyond simple belt drives. The mechanism involves granular tracking of inbound freight patterns against erratic aftermarket demand spikes rather than steady OEM cycles.

Adding analyst layers increases overhead costs that small distributors cannot absorb without scale. Without the volume of a substantial player, the supply chain complexity of 26 new SKUs covering 160,000 vehicles creates unsustainable friction. Operators must benchmark against cross-industry turns where optimization reduced cash tied in stock by significant margins, as seen in an Avaya Products and Brands solutions should prioritize tools that visualize these turn-rate variances immediately. Failure to separate slow-moving European imports from fast-turn domestic stock guarantees working capital stagnation.

Aftermarket Distribution Complexity vs OEM Linear Production Models

Aftermarket distribution manages non-linear demand spikes unlike the fixed-volume predictability of OEM assembly lines. This structural divergence forces suppliers to align with strategies like AutoZone's Mega-Hub strategy 3-billion-by-2033-driven-by-aging-vehicle-fleets-and-service-digitization. Html), prioritizing slow-moving part availability over pure velocity. Competitors such as Dorman Products compete on breadth of SKU count rather than solely on OE-specific engineering patents. Balancing broad coverage against capital efficiency without starving new launches defines the challenge.

Expanding coverage for over 160,000 vehicles requires holding diverse stock that may turn slowly. The inventory turns metric suffers if inbound freight aggregation fails to match these fragmented needs. Cloud tools help, yet human analysis remains necessary to prevent cash lock-up in static repair solutions. Failure to distinguish these models leads to excess stock in high-volume distribution centers.

About

Priya Raman, Aftermarket Category & Supply-Chain Strategist at KZMALL Auto Parts, brings over 15 years of specialized experience in parts cataloging, sourcing, and B2B distribution to her analysis of supply chain dynamics. Her daily work managing inventory economics and ACES/PIES fitment data for KZMALL's 50,000+ SKUs directly informs her perspective on strategic hiring trends like Litens Aftermarket's recent appointment. As KZMALL operates as a global single-source supplier model, Raman understands the critical pressure expanding automotive markets place on distribution networks. She connects these industry shifts to real-world operational needs, explaining why companies are prioritizing analysts who can navigate complex logistics during periods of aggressive expansion. Her expertise ensures that discussions around supply chain optimization are grounded in the practical realities of turning parts knowledge into margin for independent aftermarket buyers and owners.

Conclusion

Scaling aftermarket distribution breaks when freight aggregation strategies designed for linear OEM models collide with erratic demand spikes. Applying uniform velocity targets across 160,000+ vehicle applications causes immediate working capital stagnation, not just minor inefficiency. As thermal management lines and legacy brands merge, the risk shifts from simple stockouts to obsolescence traps in slow-moving European imports. You must decouple your inventory policies for aging fleet coverage from new launch velocity requirements immediately.

Adopt a dual-tier inventory policy by Q3 that segregates high-volume domestic stock from low-velocity imported components. Do not apply blanket turn-rate targets across diverse product lines; this approach guarantees cash lock-up in static repair solutions. Instead, mandate distinct replenishment algorithms for erratic aftermarket demand versus predictable OEM schedules. This separation prevents the dilution of capital efficiency while maintaining the breadth required for competitive coverage.

Start by auditing your top 50 slowest-moving SKUs this week to identify which ones are currently subsidized by high-velocity freight contracts. Reclassify these items into a dedicated low-frequency fulfillment lane to stop bleeding margin on unnecessary expedited shipping. This specific segmentation creates the financial headroom needed to fund broader SKU proliferation without triggering a liquidity crisis.

Frequently Asked Questions

Analysts can improve item turns by nearly 50% through targeted interventions. Historical data shows unified platforms may boost inventory turns by 200% while significantly reducing cash tied up in stock levels.

Supply chain costs have risen by 15% due to order volume increases. Analysts address this by executing inventory reduction projects that free up working capital without disrupting daily warehouse operations.

Unified technology platforms can reduce cash tied up in stock by 94%. This approach helps operators balance aggressive turn improvements with the need to maintain high service levels during expansion.

Analysts prevent stockouts by balancing turn targets against service agreements. While some platforms improve turns by 200%, operators must ensure demand forecasting keeps pace with execution speed to avoid losing sales.

Dedicated analysts focus on data-driven item turns instead of mere shipment tracking. This specialization is crucial since supply chain costs have risen by 15% due to increasing logistical complexities.