Jobbers face 2026: Balancing stock amid caution

The CFIB Business Barometer sits at 58.5, a number that tells Canadian automotive jobbers everything they need to know: caution has replaced optimism. Surviving 2026 demands we ditch passive inventory models. We need aggressive value communication and precise stock balancing. With geopolitical conflict in the Middle East pushing inflation toward 3 per cent, the era of easy margin expansion is dead.

TD Economics warns sales will retreat from 2025 highs as trade tensions and subdued growth reshape aftermarket dynamics. Volume no longer offsets rising lubricant costs or petrochemical supply shocks. Success now hinges on mastering inventory mechanics that protect cash flow without sacrificing service levels.

This piece dissects how economic uncertainty forces a hard choice between safety stock and lean principles. We analyze how Bank of Canada rate decisions directly impact the credit lines jobbers need to bridge the gap between supplier cost hikes and slower customer payments.

The Role of Economic Uncertainty in Reshaping Aftermarket Dynamics

Defining SKU Mix Shift Amid Inflationary Pressure

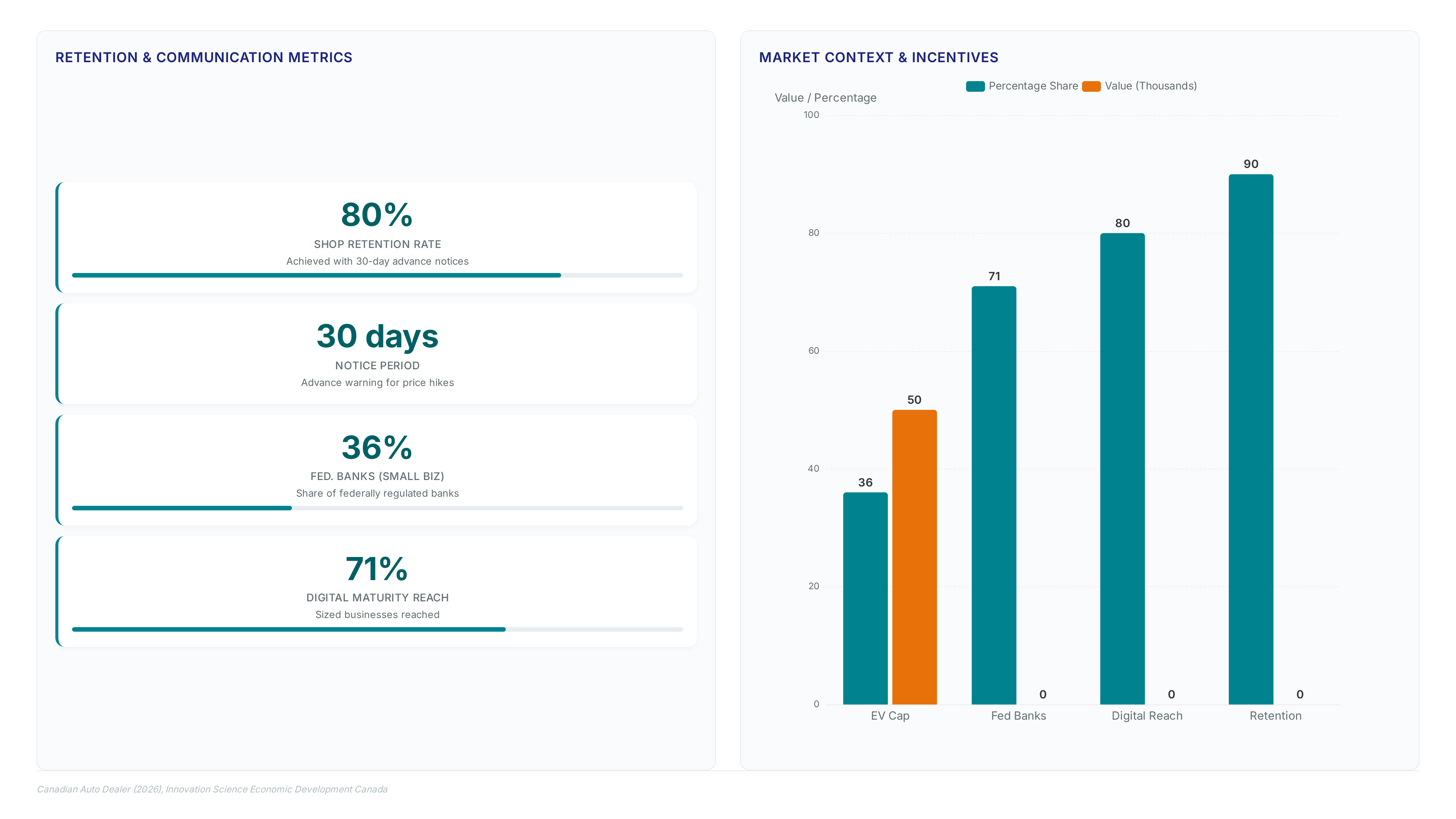

Inflation changes behavior. Consumers delay preventative maintenance, pivoting demand toward critical breakdown repairs. Jobbers holding inventory for routine service face stranded capital while repair categories surge. A CFIB Business Barometer reading of 58.5 signals that small business owners remain cautious rather than optimistic about future spending. This caution alters purchasing behavior directly. As the March CPI print tracks near 2.5 per cent, disposable income for non-necessary vehicle upkeep evaporates. Operators watching this metric see tangible compression in average repair order values at the shop level. Margin-rich maintenance SKUs turn slower. High-volume repair lines like brakes and suspension accelerate.

Aging Vehicle Parc Driving Repair-Driven Demand

Canadians are keeping cars longer. This creates a structural repair-driven demand cycle distinct from new sales volatility. The Canadian vehicle fleet now averages over 12 years old, pushing owners to extend the life of existing assets. When capital tightens, owners prioritize necessary safety components over cosmetic upgrades or preventative schedules. Data projects the national aftermarket will reach US$19 billion by 2030, driven largely by this aging inventory requiring frequent intervention.

The distribution model has simultaneously evolved from walk-in traffic to digital discovery, complicating how jobbers capture this latent volume. Operators must stock brakes and suspension lines aggressively while reducing exposure to slow-moving maintenance categories. Insufficient domestic demand remains the primary constraint for small businesses, limiting the total addressable market despite the aging fleet. Volume increases while average transaction value compresses due to consumer caution. Historical turnover rates for premium lubricants or additives become unreliable when wallets are closed. Network planning implications involve recalibrating SKU mix algorithms to weight failure-prone parts heavier than service intervals. Failure to adjust leads to stranded capital in non-necessary categories while critical repair lines face stockouts. Success requires aligning procurement cycles with breakdown frequency rather than seasonal service peaks.

Margin Erosion Risks in Cost Pass-Through Strategies

Absorbing upstream price hikes on lubricants and parts risks customer churn and immediate gross margin erosion. Manufacturers force distributors to accept higher costs, creating a squeeze where delaying price adjustments hurts profitability. This mirrors broader transport trends where carriers trim capacity as fuel economics tighten, yet automotive shops lack the scale to hedge energy exposure effectively. The policy rate holding at 2.25% limits capital access for inventory buffering, forcing reliance on cash flow that inflation consumes. Small operators face acute pressure.

One retailer accelerated capital expenditure to avoid impending tariff hikes, highlighting how trade policy volatility disrupts standard procurement cycles. Diversifying suppliers mitigates single-source price shocks while maintaining service levels. Shifting vendors introduces qualification delays that leave shelves empty during demand spikes. Operators must calculate the exact breaking point where a client switches suppliers. The additional costs from tariffs prove that waiting for stability often costs more than acting prematurely. Strategic decisions now hinge on precise timing rather than broad market sentiment.

Inside Inventory Mechanics: Balancing Safety Stock Against Lean Principles

Lean Inventory Mechanics Versus Safety Stock Buffers

Lean inventory models fail when constrained supply prevents restocking during demand spikes, forcing jobbers to hold excess safety stock. Traditional just-in-time logic assumes reliable lead times, but current market volatility renders standard reorder points obsolete for critical SKUs. Operators must recalibrate based on specific friction points hindering small business liquidity.

- Demand Volatility: Insufficient domestic demand creates unpredictable order cadences that break algorithmic forecasting.

- Upstream Costs: Grocery suppliers instating fuel surcharges signals broad logistics inflation hitting auto parts next.

- Capital Strain: Holding extra inventory ties up cash needed for digital discovery tools.

| Feature | Lean Model | Safety Stock Buffer |

|---|---|---|

| Primary Goal | Efficiency | Availability |

| Risk Profile | Stockouts during shocks | Capital stagnation |

| Best Fit | Stable supply chains | Volatile SKUs |

| Cash Impact | Low tie-up | High tie-up |

Measurable capital stagnation beats lost sales during shortages. While lean principles minimize waste, they maximize exposure to supply chain breaks. Jobbers holding zero buffer risk total category abandonment by repair shops facing their own domestic demand constraints. Strategic depth in volatile categories protects revenue when competitors cannot fill orders. This approach requires accepting lower turns on specific lines to secure overall market position. The cost of a stranded warehouse is less than the cost of an empty shelf during a surge.

Broadening Category Mix With EV and ADAS Components

Jobbers must prioritize ADAS calibration tools and hybrid components. Why? Grid upgrades for EV charging can cost between $50,000 to $500,000+, creating regional variances that delay fleet electrification. This infrastructure expense forces many commercial operators to extend internal combustion vehicle lifespans rather than transition immediately.

- Target Selection: Focus inventory expansion on tire programs, TPMS, and specialty undercar parts rather than pure EV drivetrains.

- Tooling Support: Supply repair shops with diagnostic equipment needed for existing hybrid fleets still on the road.

- Cost Modeling: Account for battery energy storage systems required for charging that cost $300 to $500 per kWh, a variable that makes rapid electrification prohibitively expensive for small fleets.

The strategic error lies in assuming high vehicle prices alone drive repair demand; the limiting factor is often the capital expenditure required to service electric platforms.

| Category Priority | Driver | Inventory Action |

|---|---|---|

| Legacy ICE | High grid upgrade costs | Increase safety stock on suspension and brakes |

| Hybrid Systems | Extended vehicle life | Add high-voltage safety gear and coolants |

| EV Specifics | Federal caps on imports | Limit SKU count to high-turn consumables |

Expanding into these categories requires capital commitment before volume materializes, creating a cash flow tension for distributors accustomed to quicker turns. Products and Brands should guide partners to view category mix expansion as a hedge against infrastructure bottlenecks rather than a direct response to current EV sales figures. The aftermarket supply chain must adapt to a prolonged transition period where older vehicles remain in service longer due to charging infrastructure economics.

Mechanics: Margin Erosion Risks in Aggressive Cost Pass-Through

Aggressive cost pass-through fails when shop customers push back against price hikes, forcing jobbers to absorb increases that erode margin. Manufacturers passing through costs on lubricants place distributors in a squeeze where delaying adjustments bleeds gross profit immediately. When wallets tighten, consumers defer preventative maintenance and wait for breakdowns, compressing average repair orders for local garages. This behavioral shift reshapes the required SKU mix toward emergency repair lines while slowing turns on margin-rich maintenance categories.

| Risk Factor | Consequence | Operational Response |

|---|---|---|

| Absorbing Costs | Immediate margin erosion | Implement staged pricing increases |

| Aggressive Pass-Through | Customer churn | Equip shops with value scripts |

| Deferred Maintenance | Compressed order size | Shift inventory to repair parts |

Jobbers must equip repair shops with value-communication tools to justify price increases to end consumers rather than silently absorbing the hit. Without this support, the cycle of deferral accelerates, leaving distributors holding slow-moving stock in a constrained demand environment.

Executing Value Communication to Retain Shops During Price Hikes

Counter staff must reframe price objections using talking points derived from tariff-induced price increases that force equipment replacement cycles. Jobbers supply counter-ready POS materials illustrating how supply constraints drive parts costs higher than historical norms. Training focuses on explaining that delayed maintenance increases long-term repair expenses for consumers holding vehicles longer.

The distribution environment has shifted from abundant inventory to constrained supply, making reliable availability a premium service attribute. Shops compete against national chains by offering immediate part access rather than lowest sticker price. Jobbers holding a significant share of the market use this proximity to justify margin retention.

However, providing training resources requires jobbers to absorb short-term educational costs without immediate revenue lift. Staff must articulate why domestic manufacturing incentives alter component pricing structures differently than imported goods. The limitation lies in consistent message delivery across diverse counter personnel skill levels. Operators ignoring this communication gap lose shop partners to big-box competitors offering identical SKU counts but superior narrative support.

Executing Dedicated Account Management for National Key Accounts

Securing a substantial sum aspx? G=126fffe9-4425-4512-830c-bd624ef788c0) vehicle parc units requires dedicated account managers who deploy EDI integrations to lock in fleet supply chains. National operators face distinct liquidity constraints compared to independent garages, necessitating structured retention protocols beyond standard price lists. Jobbers must assign senior representatives to multi-location groups, ensuring custom SKU assortments align with specific regional repair volumes. This approach mirrors the strategic consolidation seen in finance, where institutions like National Bank of Canada f/national-bank-of-canada/management) use scale to stabilize revenue during market volatility. Without such focus, large accounts bypass jobbers for direct manufacturer contracts that offer rigid but predictable pricing.

- Implement custom delivery windows that align with fleet operator maintenance cycles rather than generic drop times.

- Deploy counter-ready POS materials specifically designed for national branding consistency across all shop locations.

- Establish quarterly business reviews using data analytics to forecast parts demand based on local vehicle aging trends.

The limitation of this model is the high overhead cost; sustaining a dedicated team demands volume that smaller distributors cannot match. Consequently, only well-capitalized jobbers can afford the field presence required to court these accounts effectively. This creates a bifurcation where mid-sized players lose anchor clients to larger competitors who absorb the service cost. Operators ignoring this shift risk becoming commodity suppliers for smaller shops while losing high-volume contracts. The market rewards those who treat account management as a technical integration of logistics and sales rather than a relationship exercise. Failure to embed structured programs results in immediate margin compression as fleets consolidate their vendor lists.

Checklist for Preventing Churn During Auto Parts Price Increases

Validate talking points against current tariff-induced price increases before communicating cost adjustments to repair shop partners. Jobbers must verify that counter staff explain supply constraints using data on forced early equipment replacement rather than generic inflation claims. Blunt price notifications without context trigger customer defection to competitors offering marginally lower sticker prices.

| Strategy Component | Execution Tactic | Risk if Omitted |

|---|---|---|

| Value Narratives | Deploy POS materials highlighting parts scarcity | Shops perceive hikes as greedy rather than necessary |

| Category Mix | Expand into undercar and diagnostic tools | Revenue gaps emerge as maintenance deferral rises |

| Account Structure | Assign dedicated managers for multi-location groups | National accounts consolidate purchases with large distributors |

Expand category mix beyond consumables to include diagnostic equipment and specialty undercar parts, offsetting volume loss in routine maintenance. Consumers holding vehicles longer due to high replacement costs create sustained demand for repair-heavy SKUs. This shift requires inventory capital but protects gross margin when lubricant volumes contract. Equip sales teams with specific scripts addressing the policy rate. Operators ignoring this macro signal fail to align their credit terms with customer cash flow realities. Products and Brands recommends auditing account structures quarterly to ensure dedicated account management for high-volume clients facing similar pressures. Neglecting these validation steps allows competitors to capture market share during periods of economic stress. The cost of churn exceeds the effort required to maintain transparent communication channels with shop owners.

Implementing Expansion Plays for Tires, TPMS, and Fleet Programs

Defining Structured Fleet Programs and EDI Integration

A structured fleet program for jobbers requires EDI integration to synchronize inventory data with multi-location operators, eliminating manual order errors that plague high-volume accounts. Without this technical backbone, national accounts cannot scale service delivery across dispersed repair bays. The implementation begins with mapping customer-specific SKU codes to the distributor's master catalog, a process that demands precise configuration of purchase order fields to ensure smooth transaction flow.

- Configure EDI 850 transaction sets to accept automated purchase orders directly from fleet management software.

- Map vendor part numbers to customer-specific aliases to prevent rejection at the receiving dock.

- Expand beyond traditional hard parts by integrating tire programs and ADAS calibration tools to capture demand from a vehicle parc averaging over 12 years.

- Stock volatile SKUs targeting suspension and undercar components, as consumers defer new purchases when new vehicle sales decline versus prior years.

- Implement counter sales training that uses value-communication scripts to explain repair necessity over replacement, addressing the hesitation seen in current consumer confidence metrics.

- Acquire specialized diagnostic equipment capable of servicing hybrid systems, noting that federal incentives still apply to vehicles under specific transaction value caps while exemptions support domestic manufacturing.

- Counter teams require deferral scripts grounded in specific infrastructure cost barriers to justify repair over replacement.

- Train staff to cite grid upgrades costing up to half a million dollars as proof that fleet electrification remains distant for many operators.

- Distribute POS materials highlighting that battery storage systems demand substantial capital, extending the service life of current internal combustion vehicles.

- Validate talking points against the reality that federal caps limit incentives, leaving older vehicles as the primary revenue source for shops.

- Equip sales reps with category mix data showing repair demand outpaces new sales during economic contraction.

| Conversation Anchor | Technical Constraint | Shop Benefit |

|---|---|---|

| Infrastructure Cost | High grid upgrade expenses | Justifies repair investment |

| Fleet Strategy | Delayed electrification timelines | Extends customer retention |

| Inventory Focus | Aging vehicle parc growth | Increases parts volume |

Shops ignoring these technical constraints risk losing margin to competitors who frame repairs as strategic asset preservation. Operators must avoid generic inflation narratives and instead deploy specific data on charging infrastructure. This approach transforms the counter interaction from a transactional dispute into a consultative partnership focused on asset longevity.

About

Dmitry Volkov, Senior Automotive Technical Writer at KZMALL Auto Parts, brings necessary technical clarity to the complex challenges facing today's automotive jobber. In his daily role, Volkov translates complex engineering data and manufacturing standards into actionable insights for counter professionals, a skill critical when navigating the current economic turbulence driven by Middle East conflicts. As global instability drives up costs for lubricants and replacement parts, Volkov's expertise in ACES/PIES fitment data and supply chain dynamics allows him to contextualize how inflation impacts inventory strategy. Working with KZMALL's extensive catalog of over 50,000 SKUs, he understands the delicate balance jobbers must maintain between rising procurement costs and cautious consumer sentiment. His analysis bridges the gap between macroeconomic indicators, such as the CFIB Business Barometer, and the practical realities of managing a parts counter, offering industry readers a grounded perspective on seizing opportunity amidst market volatility.

Conclusion

Scaling this consultative model reveals a critical fracture in working capital efficiency when inventory turnover slows due to tariff-induced supply chain friction. The operational burden shifts from mere stock availability to financing the gap between delayed restocking and immediate customer demand, a pressure point exacerbated by restricted credit access. While the market expands, margins will compress for jobbers who fail to differentiate their value proposition beyond price, especially as trade tensions dampen new vehicle sales volume in 2026.

Jobbers must immediately pivot inventory strategies to prioritize high-turn repair components for vehicles exceeding twelve years of age, explicitly deprioritizing speculative stock for emerging EV segments until infrastructure costs stabilize. This reallocation should occur within the next quarter to capture the structural repair demand before competitors lock in supplier agreements. Do not wait for federal incentives to clarify; the math on grid upgrades alone dictates a prolonged reliance on internal combustion maintenance.

Start by auditing your current inventory mix against the age profile of vehicles in your specific trade area this week. Identify slow-moving SKUs tied to newer technologies and liquidate them to fund immediate purchases of aging-fleet essentials, ensuring your cash flow aligns with the reality of deferred fleet electrification.

Frequently Asked Questions

An Alberta business owner reported unexpected tariff exposure costs reaching $7,000. This sudden expense forces premature equipment purchases that drain essential liquidity needed for daily inventory operations during these uncertain economic times.

Data projects the national aftermarket will reach US$19 billion by 2030. This growth is driven largely by an aging vehicle fleet requiring frequent repair interventions rather than new car sales.

Consumers delay preventative maintenance because inflation erodes disposable income for non-necessary vehicle upkeep. This caution shifts demand toward critical breakdown repairs while margin-rich maintenance SKUs turn significantly slower in the current market.

Jobbers must stock repair lines aggressively while reducing exposure to slow-moving maintenance categories. Ignoring this shift leaves distributors overexposed to stranded capital while understocked for urgent repair demand.

A CFIB Business Barometer reading of 58.5 signals that small business owners remain cautious rather than optimistic about future spending. This directly alters purchasing behavior and compresses average repair order values.