Aftermarket reality: 38% demand cost help now

Genuine OE brands still command over 60% of parts purchases, yet MacKay & Company data reveals a distinct fracture in channel loyalty as engine distributors aggressively pivot to non-OE alternatives. The 2026 DataMac U. S. Distribution Report confirms that while Original Equipment dominance remains the baseline, the commercial vehicle aftermarket is no longer a monolith but a battleground set by parts availability crises and divergent sourcing strategies.

Channel dynamics are reshaping inventory logic. HDD specialists and independent garages are capturing increased market share from subsequent owners desperate for service options. The analysis dissects the 2025 pricing mechanics, where a moderated 4.0% average increase masked severe channel-specific variances ranging from 3.3% to 4.6%, forcing distributors to choose between margin preservation and volume retention. The report exposes that 38% of distribution channels now demand manufacturer intervention on cost structures, surpassing even parts availability as the primary request for support despite supply chain headlines. As the aging fleet drives demand, successful operators are those adapting strategic inventory models to accommodate the shift away from strict OE dependency, recognizing that warranty expiration triggers an immediate migration toward price-sensitive independent garages and specialized distributors.

The Role of OE and Aftermarket Channels in Modern Distribution

Defining OE and Aftermarket Channels in Heavy-Duty Distribution

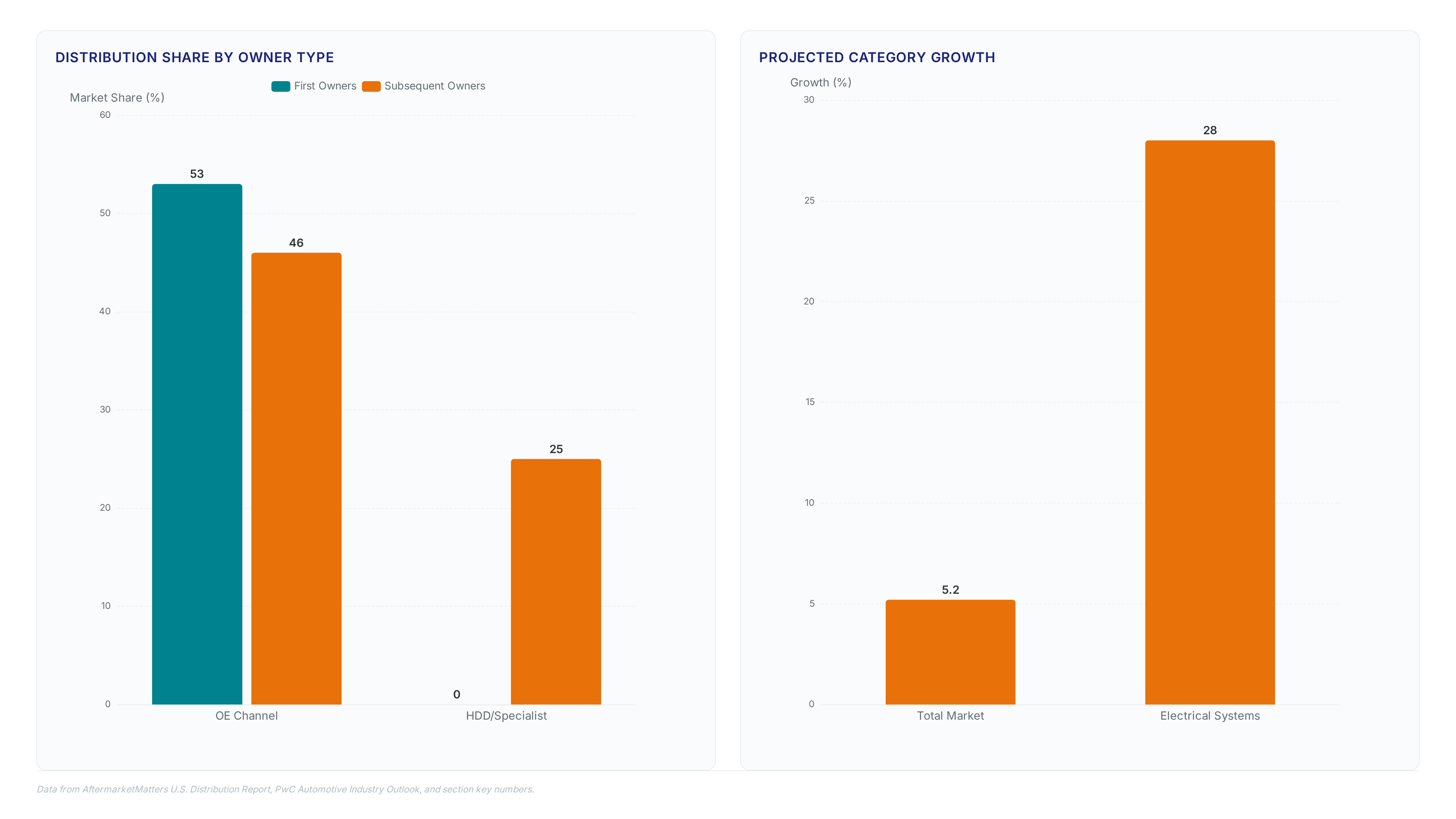

Genuine OE brands command over 60% of all parts purchased for resale or installation across the sector. Dealers and engine distributors secure the largest portions of this volume within traditional networks. Specialized heavy-duty distributors are now adopting more aftermarket components, disrupting previous hierarchies specialized heavy-duty distributors. Traditional warehouse distributors maintain a dominant share of independent aftermarket growth. E-commerce portals lag notably at a significant share Traditional warehouse distributors.

- OE Dealers Genuine Parts 46%

- HDD Specialist Mixed Sourcing 25%

- Independent Garage Aftermarket 14%

- Other Channels a small share

Ownership Lifecycle Shifts: OE Adoption from First to Subsequent Owners

Vehicle age dictates sourcing strategy as genuine OE brands lose ground to cost-sensitive alternatives. This decline correlates directly with warranty expiration and asset depreciation cycles. Independent operators prioritize cash flow over brand fidelity once initial coverage lapses. The financial pressure forces a reevaluation of parts availability versus premium pricing structures. These facilities offer lower labor rates that offset the perceived risk of non-OE components. Fleet managers often mandate independent sourcing to meet strict operating budgets during later lifecycle stages. The shift reveals a structural tension between manufacturer loyalty programs and real-world repair economics. Operators sacrificing brand consistency gain immediate cost relief but risk long-term residual value ambiguity. This constraint defines the modern distribution environment where price sensitivity overrides original equipment mandates. Data points to a clear migration pattern as assets age beyond factory support windows.

Channel Divergence: Dealer OE Loyalty vs Specialist Aftermarket Adoption

Dealers and HDD specialists tightened OE parts reliance in 2025 while engine distributors expanded non-OE inventory. This divergence creates a bifurcated supply chain where channel strategy dictates component authenticity. Operators prioritizing warranty compliance face limited options as independent channels pivot toward generic substitutes. This shift forces specialized heavy-duty distributors. The consequence is a fragmented parts availability environment where identical vehicle models receive different component grades based solely on the service channel selected. Fleet managers must audit service invoices to verify component provenance, as the visual distinction between OE and aftermarket parts diminishes in complex assemblies.

The HDD specialist channel captures a small average parts market share for subsequent owners, exceeding the 23% held for new vehicle owners. This shift indicates that warranty expiration directly drives volume toward non-OE channels. A key tension exists between parts availability and cost control; while 38% of channels cite pricing pressure as a top challenge, 34% prioritize availability above all else. Operators must balance immediate repair needs against long-term supplier relationships. The DataMac study gathered insights from 260-plus businesses to map these evolving behaviors 260-plus businesses Ignoring the HDD specialist migration risks inventory obsolescence as fleets age out of warranty coverage.

Inside Sourcing Behavior and Pricing Mechanics for 2025

The 4.0% Average Price Rise vs 2022 Inflation Spike

The 4.0% average price rise in 2025 reflects moderated inflationary pressure compared to the 10.2% spike recorded in 2022. This specific mechanical driver stems from stabilizing raw material costs rather than reduced demand, as fluctuating raw material prices remain a primary challenge for component availability. Operators observe a distinct divergence where commercial heavy-duty pricing trails the broader automotive sector, which saw aftermarket price inflation reach 12.3%. The gap suggests fleet managers successfully used long-term contracts to buffer immediate cost shocks. Dealers absorbing higher OE parts costs contrast sharply with independent garages using non-OE alternatives to maintain margin.

Operators must recognize that price competition among manufacturers directly impacts the durability of sourced components. The structural shift toward diversified sourcing means profit margins now depend on navigating these variances rather than absorbing them. Failure to audit channel-specific pricing exposes fleets to hidden costs that exceed the nominal savings of non-OE alternatives. Strategic procurement requires isolating these variances before contract renewal cycles lock in unfavorable terms.

Strategic Inventory Adaptation for Evolving Channel Dynamics

Defining Strategic Inventory Adaptation Amid Channel Volatility

Balancing parts availability challenges Operators cannot simply stock deeper; they must stock smarter by aligning inventory mix with the specific shift away from genuine OE dominance as vehicles age. This mechanical reality forces a divergence where traditional warehouse distributors, holding the majority of growth share, must optimize routing logic to serve fragmented demand. The Integration Hub model demonstrates how normalizing orders across multiple sales channels into a single ERP system reduces manual handling errors during peak volatility.

Fluctuating raw material prices directly impact the stability of aftermarket product pricing, creating a volatile environment for long-term planning. The broader market projects steady expansion toward a $500 billion valuation by 2029, yet immediate survival depends on mitigating the friction caused by these input cost variations. A sharp limitation emerges here: adapting inventory solely for cost ignores the reliability gap often found in cheaper alternatives, risking fleet uptime. Successful adaptation means accepting that channel dynamics now dictate component authenticity rather than manufacturer mandates alone.

Using Vehicle Aging Trends for Aftermarket Stocking Decisions

Inventory mix adjustments must target the projected 5.2% growth driven specifically by an aging vehicle fleet requiring frequent repairs. Operators should prioritize electrical system upgrades, as sales in this category are anticipated to rise by 28% due to increasing vehicle complexity. Simultaneously, stocking performance tuning software addresses a distinct 22% surge in demand for software-set modifications that legacy supply chains often ignore. Genuine brands dominate initial ownership, but the shift to independent channels for subsequent owners demands a diversified portfolio to capture value. Failure to adapt inventory logic to these aging profiles results in stranded capital on slow-moving OE parts that older fleet operators no longer purchase. Distributors must align procurement with the mechanical reality that warranty expiration triggers an immediate pivot toward aftermarket solutions. This transition requires discarding static stocking models in favor of flexible lists that reflect the specific age bracket of the local customer base.

Mitigating Margin Erosion from Intense Price Competition

Cost and pricing pressure ranked as the No. 3 challenge of 2025, yet it drives the most aggressive requests for manufacturer aid. Operators face a structural trap where intense price competition forces suppliers to reduce costs, often leading to compromises in component quality to maintain margins. This flexible creates a false economy where short-term margin preservation accelerates long-term liability through premature part failure.

The industry cites fluctuating raw material prices as a primary challenge impacting the availability and pricing of aftermarket products, making static pricing models obsolete. A improved approach involves formalizing cost-sharing agreements that tie inventory depth to volume commitments rather than spot pricing. The constraint is clear: without contractual protection against fluctuating costs , distributors absorb the full shock of upstream volatility. Manufacturers must provide tiered pricing structures that reflect actual market stress rather than historical averages. Survival depends on shifting from transactional purchasing to strategic partnership frameworks that distribute risk.

Steps for Improving Parts Availability and Resolving Supply Gaps

Defining Parts Availability Gaps Amid Raw Material Volatility

Fluctuating raw material prices create the primary mechanism for availability gaps by forcing suppliers to halt production lines when input costs spike unpredictably. Unlike general inflation, raw material swings cause sudden stops rather than gradual price creep, leaving inventory shelves empty despite high warehouse capacity.

- Monitor commodity indices daily to anticipate supply shocks before they hit distribution centers.

- Diversify sourcing beyond single-region regional distribution centers to mitigate localized material shortages.

- Implement flexible safety stock algorithms that adjust reorder points based on material cost volatility rather than just sales velocity.

The limitation is that holding extra inventory to buffer against these gaps increases exposure to the very cost pressures driving the market shift. Operators must balance the risk of stockouts against the capital cost of holding excess inventory during periods of price instability. Products and Brands recommends configuring alert thresholds to trigger sourcing reviews when material costs move outside historical bands. This approach prevents reactive panic buying while ensuring critical parts remain available for aging fleets requiring immediate repair.

Implementing Stocking Strategies for Electrical Upgrades and Tuning Software

Distributors must prioritize zonal architecture components to address the decentralized electrical structure now standard in commercial fleets. This technical shift requires stocking specific interface modules rather than generic wiring, as OEMs commit to new E/E structures that legacy inventories cannot support. The operational risk involves holding obsolete harnesses while demand migrates to zone-gateway controllers. Operators should execute the following inventory adjustments to capture growth in non-OE segments:

- Reallocate shelf space toward performance tuning software licenses to match surging demand for software-set vehicle modifications.

- Stock diagnostic tools capable of flashing centralized head units where automotive OS software typically resides.

- Reduce deep inventory of mechanical wear items in favor of high-turnover electronic sensors.

- Implement version-control protocols for software SKUs to prevent compatibility errors during installation.

The limitation of this strategy is the reliance on stable digital supply chains, which remain vulnerable to semiconductor constraints. Unlike mechanical parts, tuning software cannot be expedited via air freight once a supply gap occurs. Products and Brands recommends verifying vendor update cycles before committing capital to software-heavy SKUs.

Avoiding Quality Compromises When Countering Intense Price Competition

Intense price competition. This pressure manifests as subtle material substitutions in critical braking systems that evade initial visual inspection but accelerate wear rates under heavy load. Operators must implement strict vendor validation protocols to filter out substandard inventory before it enters the supply chain.

- Mandate third-party metallurgical testing for all non-OE brake and lighting components.

- Audit supplier compliance with new regulatory oversight to avoid fines that erase thin profit margins.

- Reject bids lacking traceable raw material certifications despite lower unit pricing.

The cost of fluctuating raw material prices tempts manufacturers to switch alloys, yet this volatility makes long-term reliability forecasting impossible without verified data. Distributors relying on Products and Brands for sourcing gain a structural advantage by accessing audited supply lines that resist these quality degradations. The hidden consequence of accepting cheaper parts is a surge in warranty claims that outweighs the initial procurement savings.

About

Anna Petrova serves as a B2B Auto Parts Market Analyst at KZMALL, where she specializes in market sizing and competitive dynamics within the global automotive aftermarket. Her daily work involves translating complex distribution data into actionable sourcing strategies, making her uniquely qualified to interpret the findings of the 2026 DataMac U. S. Distribution Report. As KZMALL operates a massive wholesale platform covering over 50,000 SKUs for light- and heavy-commercial vehicles, Petrova constantly navigates the very channel shifts the report highlights. Her analysis of MacKay & Company's survey of 260-plus businesses directly informs KZMALL's single-source supplier model, ensuring their catalog aligns with evolving dealer and distributor needs. By connecting high-level industry trends to practical inventory decisions, Petrova bridges the gap between raw market data and the operational realities faced by parts buyers in the commercial vehicle aftermarket.

Conclusion

The current distribution model fractures when warranty liabilities from substandard components exceed the thin margins gained through aggressive discounting. As the commercial fleet ages, the operational burden shifts from simple inventory turnover to rigorous liability management, where a single batch of unverified brake components can erase annual profits. Relying on legacy sourcing habits without enhanced validation protocols creates a fragile supply chain that cannot withstand regulatory scrutiny or the demands of older, high-mileage vehicles.

Distributors must immediately pivot to a verified-only procurement strategy for all safety-critical systems by the end of Q3. This transition requires rejecting any supplier unable to provide real-time metallurgical certification, regardless of their unit price advantage. The window for tolerating opaque supply chains has closed; survival depends on establishing traceable quality gates that prioritize long-term fleet reliability over short-term cost reduction.

Start this week by auditing your top five non-OE brake suppliers and demanding current material compliance certificates for their last three shipments. If they cannot produce these documents within 48 hours, remove their SKUs from your active purchase orders immediately to prevent contaminated inventory from entering your warehouse.

Frequently Asked Questions

Parts pricing rose an average of 4.0% in 2025, reflecting moderated inflation compared to past spikes. This increase varies across distribution channels, ranging from approximately 3.3% to 4.6% based on specific retail sales mixes.

Independent garages hold a 14% market share for parts sold to subsequent owners, doubling their volume from new vehicle transactions. This growth reflects increased price sensitivity as vehicles age and leave warranty coverage periods.

While parts availability is a top challenge, 38% of distribution channels specifically call for greater manufacturer support to manage ongoing cost pressures. This demand surpasses requests for help with labor constraints or supply chain logistics issues.

The HDD specialist channel captures a 25% average parts market share for subsequent owners, exceeding the portion held for new vehicle owners. This shift indicates warranty expiration directly drives volume toward non-OE channels significantly.

Genuine OE brands account for over 60% of all parts purchased for resale or installation across the commercial vehicle sector. Dealers and engine distributors currently hold the largest shares among all available distribution channels today.