Independent repair shops beat dealerships on value

Of 11,670 repairs tracked by Consumer Reports, independent shops consistently outperform dealerships in member satisfaction and value. The data confirms that independent repair shops offer superior cost efficiency and service quality compared to franchise competitors, effectively dismantling the myth that dealership service departments provide necessary expertise for older vehicles. Vehicle owners paying out of pocket gain no advantage from inflated dealership labor rates when local providers deliver higher scores across critical performance metrics.

Warranty constraints often mislead consumers into paying premium prices at franchised service centers despite lacking legal necessity. The 2023 Summer Survey reveals stark labor rate disparities, with members rating facilities on twelve specific attributes including honesty, price accuracy, and communication. Note that the survey excludes routine maintenance and collision damage to focus strictly on unexpected mechanical failures and electronic defects.

Strategic provider selection relies on survey methodology that randomly selected one repair per shop per member to ensure statistical validity. Analyzing feedback from 10,973 members shows service quality ratings drop significantly at dealerships due to poor price negotiation and lack of perks. This evidence-based approach guides drivers toward maximizing vehicle longevity without succumbing to unnecessary markups or restrictive service contracts.

Defining the Automotive Repair Environment and Warranty Constraints

Factory Warranty Repair vs Routine Maintenance Definitions

Distinguish between a factory warranty repair, which corrects unexpected defects, and routine maintenance, which prevents wear through scheduled service. This technical distinction dictates coverage eligibility and determines whether a vehicle owner must visit a dealership or can choose an independent facility. Repairs address mechanical or electronic failures caused by broken parts. Maintenance covers predictable tasks like oil changes, fluid top-offs, and wiper replacement.

Consumer Reports published survey results on March 20, 2024, based on data collected from its members regarding automotive service facilities. The study focused exclusively on repairs paid for out of pocket. Recall repairs, routine maintenance, tire damage or replacement, and collision damage fell outside the scope.

When Dealerships Are Mandatory for Sensor Calibration

Dealerships remain the recommended option for repairing and calibrating safety and driver aid sensors, particularly for parts specific to the vehicle. Modern vehicles embed radar and lidar units in bumpers that must align precisely with the car's computer to enable automatic emergency braking and adaptive cruise control. These sensors often need to be recalibrated with special equipment so that the car's computer knows where the car is in relation to other cars and objects.

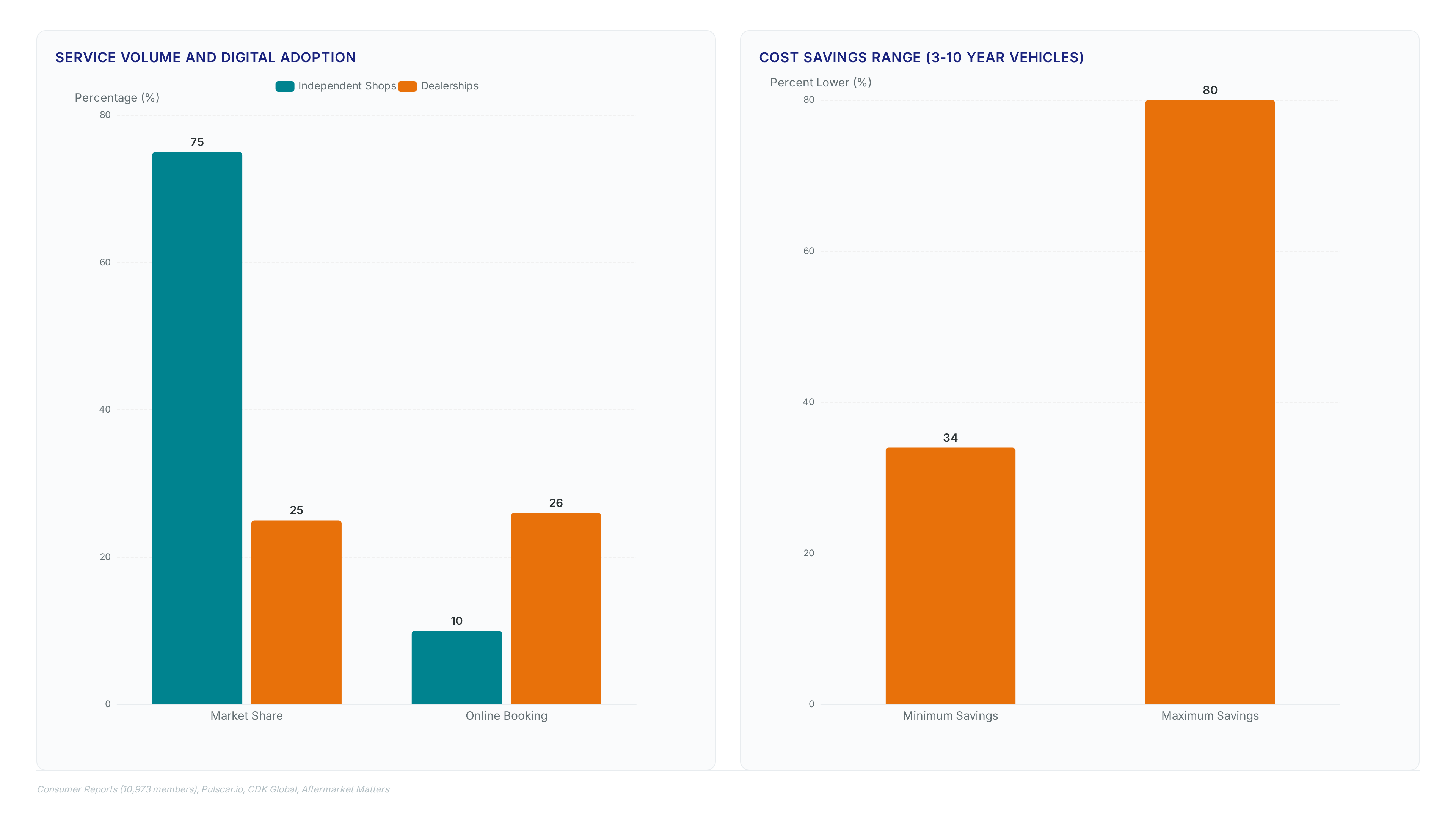

While independent shops perform roughly 75% of aftermarket work, complex electronic defects frequently fall outside their equipment scope. Software updates lacking over-the-air capability also mandate dealer intervention.

Comparing Service Quality and Labor Rates Across Shop Types

Defining Service Tiers: Dealerships vs Independent Shops vs Chains

Dealership service departments function as substantial revenue centers, whereas independent facilities often use former dealership technicians to deliver comparable work at reduced costs. Chains specializing in tires provide competitive pricing on specific components but frequently overlook the overall condition of the vehicle during broader inspections.

| Feature | Dealership | Independent Shop | Chain |

|---|---|---|---|

| Technician Source | Factory-trained | Former dealership staff | Mixed experience levels |

| Parts Strategy | Original equipment | Aftermarket or OEM request | Volume-sourced |

| Primary Focus | Brand-specific complexity | General repair breadth | High-volume commodities |

Independent operators consistently achieve higher marks for communication regarding the repair process compared to their franchised counterparts. Clear dialogue prevents unnecessary upsells that inflate final invoices. While tire-focused chains excel at commoditized tasks like alignments, they rarely possess the diagnostic depth required for complex engine management issues.

The operational definition of each tier reveals a hidden tension between specialized brand knowledge and complete vehicle care. Dealerships prioritize manufacturer protocols, while independents focus on extending vehicle longevity through flexible parts sourcing. Owners of older vehicles benefit most from this flexibility, as independent shops are more likely to negotiate labor rates or source cost-effective alternatives. Conversely, newer cars under warranty remain tethered to dealerships due to strict compliance requirements. Understanding these structural differences allows car owners to select a facility that matches their specific mechanical needs rather than defaulting to the most expensive option.

Applying Car Age and Brand Data to Shop Selection

Vehicle age serves as the primary predictor for selecting a repair facility over brand loyalty alone. Data indicates that while 80 percent of drivers with 2023 models visit dealerships, only 18 percent of 2000 model owners do the same. This sharp decline reflects diminishing returns on factory training as vehicles exit warranty coverage periods. Brand specificities further complicate this decision matrix for consumers seeking value.

Tesla owners exhibit the highest dealership reliance at 89 percent, likely due to specialized software dependencies. Conversely, Dodge owners visit dealerships at just 29 percent, suggesting confidence in independent shops for domestic brands. These disparities highlight how perceived technical complexity influences service location choices more than actual mechanical needs.

| Metric | New Model Strategy | Aged Model Strategy |

|---|---|---|

| Primary Venue | Dealership | Independent Facility |

| Labor Cost | High Premium | Market Competitive |

| Tooling Need | Proprietary Software | General Diagnostics |

| Parts Source | OEM Mandatory | Aftermarket Optional |

Operators must recognize that specialty tools for newer models often remain exclusive to franchised outlets initially. A technical limitation for some independent shops is the potential lack of specific, brand-new specialty tools required for the very latest vehicle models, which large dealerships are more likely to stock immediately upon release specialty tools. This gap narrows significantly as vehicles age and aftermarket support matures. The logical switch point occurs when proprietary diagnostic access no longer dictates repair success. Owners of older vehicles gain little from dealership overhead once standard OBD-II interfaces suffice for troubleshooting. Strategic shop selection maximizes value by aligning facility capabilities with actual vehicle requirements rather than habit.

This dramatic variance stems primarily from overhead structures rather than parts availability, as independent technicians can purchase OEM parts directly from manufacturers. Dealerships maintain higher labor rates to subsidize specialized brand training and proprietary diagnostic tools required for warranty work. Conversely, independent shops often employ former dealership staff who bring factory-level expertise without the associated facility costs.

Economic pressure drives declining consumer spend toward cost-efficient options, favoring independents who offer flexible parts sourcing strategies. While tire-specialty chains provide convenience for alignments and exhaust work, they frequently miss broader mechanical issues during limited inspections. The infrastructure cost of diagnostics is often lower at independents who prioritize real evaluation over parts guessing, potentially saving money on unnecessary replacements. However, this cost advantage requires the vehicle owner to verify technician credentials, as experience levels vary more widely outside the franchise system. Consumers increasingly opt for independent aftermarket services to mitigate expenses without sacrificing technical quality. The strategic choice involves balancing the peace of mind from brand-specific certification against the immediate financial relief of third-party labor rates.

Strategic Selection of Repair Providers for Maximum Value

Defining Trustworthy Repair Shops Through Consistent Maintenance

Establishing a relationship through routine maintenance at a single facility creates a verifiable service history that aids diagnostic accuracy. Ibbotson advises that getting routine maintenance done at the same place consistently allows mechanics to identify developing problems before they become expensive issues. This continuity distinguishes thorough repair facilities from transactional quick-service chains, which often lack the capability for complex diagnostics beyond basic fluid swaps.

Independent shops frequently outperform dealerships in communication quality regarding the repair process, supporting greater owner confidence over time. Survey respondents rated these independent providers higher for explaining technical details compared to franchise counterparts. A longitudinal analysis of over 121,000 vehicles confirms that consistent care patterns correlate with higher satisfaction scores across both independent and franchise models. Owners who avoid fragmenting their care across multiple providers benefit from technicians who recognize subtle changes in vehicle behavior.

| Provider Type | Routine Capability | Complex Repair Depth |

|---|---|---|

| Quick-Service Chain | High | Low |

| Independent Shop | High | High |

| Dealership | High | Highest |

The strategic value lies in the provider's ability to contextualize new faults against past performance data. Without this baseline, every symptom appears as an isolated incident rather than part of a degradation curve.

Applying Vehicle Age to Dealership vs Independent Shop Decisions

Vehicle age dictates the optimal repair venue more reliably than brand loyalty or owner habit. While 80 percent of drivers with 2023 models visit dealerships, this behavior shifts drastically as cars exit warranty coverage. The data reveals that only 18 percent of owners with model-year 2000 vehicles seek dealer service, preferring the cost efficiency of third-party providers. This transition point represents a critical financial decision for long-term asset management.

Independent facilities frequently provide service quality matching factory standards while charging significantly less for labor. The trade-off involves access to proprietary diagnostic software, which remains a barrier for complex electronic faults in newer models. However, for mechanical repairs on aging vehicles, the factory training advantage diminishes in value relative to the price premium.

| Decision Factor | Newer Vehicle Strategy | Older Vehicle Strategy |

|---|---|---|

| Primary Driver | Warranty compliance | Cost minimization |

| Technician Type | Factory-certified specialist | Generalist expert |

| Parts Sourcing | Mandatory OEM | Aftermarket or requested OEM |

Operators should establish relationships with local providers before substantial failures occur to ensure diagnostic continuity. This approach allows technicians to identify developing issues early, preventing minor defects from becoming catastrophic failures. The consequence of delaying this selection is often emergency decision-making under duress, which rarely yields optimal financial outcomes.

Checklist for Verifying Technician Credentials and Parts Options

Start by asking if the shop verifies inputs and reproduces symptoms before recommending repairs, a standard that prevents misdiagnosis from error codes alone diagnostic process. Confirm whether technicians hold current ASE certifications or manufacturer-specific training credentials the to your vehicle's complexity. Request a written policy on parts selection, specifically asking if they source aftermarket components or original equipment based on your preference. Globally, 57% of consumers now prefer independent aftermarket parts to mitigate rising repair costs consumer preference. This shift reflects an increase in demand for non-OE options as owners seek value cost trend.

| Verification Step | Question to Ask |

|---|---|

| Training Background | Are techs former dealership employees? |

| Parts Sourcing | Can I choose factory versus aftermarket? |

| Diagnostic Method | Do you test before replacing parts? |

| Warranty Terms | What guarantees cover the labor performed? |

Independent shops often match dealer quality while offering flexibility on parts that chains cannot provide. Ibbotson advises establishing a relationship through consistent routine maintenance to build trust and ensure accurate historical records. InterLIR recommends verifying these credentials annually to maintain control over your service history and long-term vehicle value.

Navigating Cost Estimates and Resolving Service Disputes

Defining Cost Drivers: Aftermarket Parts vs Factory Originals

Inaccurate repair estimates often stem from the initial assumption of using factory-original components rather than functionally equivalent aftermarket alternatives. Aftermarket parts provide a viable cost-reduction strategy, yet many vehicle owners remain unaware they can explicitly request these options during the estimate phase. Independent shops have access to purchase OEM (Original Equipment Manufacturer) parts, meaning cost differences are often driven by labor rates and overhead rather than exclusive parts availability.

The tension arises because while dealerships apply factory-original parts that are often best for specific vehicle requirements, independent shops consistently receive the highest scores for satisfaction with price.

- Ask the estimator to itemize parts by manufacturer origin.

- Specify acceptance of certified aftermarket components for non-safety items.

- Request a revised quote comparing factory versus alternative pricing.

Securing written confirmation of parts selection helps resolve potential disputes regarding estimate accuracy later.

Negotiating Repair Costs Using Shop Specialization Data

- Identify routine component swaps like tire installation or exhaust work where national chains excel.

- Request written estimates from these specialized providers to establish a competitive baseline price.

- Present the lower quote to local independent facilities, which possess greater pricing flexibility than franchise models.

Independent shops are statistically the most likely venue to bargain over price, making them receptive to this data-driven approach. Economic pressure drives many consumers toward cost-efficiency, creating an environment where shops actively compete for business through adjusted labor rates. While chains may offer convenience for specific commodities, Consumer Reports notes that chains specializing in quick services have limited capabilities compared to dealerships or independent shops for most repairs.

Owners must balance immediate savings against the risk of fragmented maintenance records that complicate future troubleshooting efforts.

Risks of Limited Diagnostic Scope at Tire Chains

Facilities that specialize in quick oil changes or tire services have limited capabilities compared to full-service repair shops. Ibbotson advises that while these chains can be convenient, dealerships or independent shops are improved for most repairs because their mechanics can get to know your car and keep an eye on developing problems before they become bigger, more expensive issues. Establishing a relationship with a shop that performs consistent routine maintenance allows staff to identify developing problems early.

- Request a full vehicle inspection report, not a tire viability check.

- Verify if the technician holds credentials beyond wheel service certification.

- Cross-reference findings with a generalist mechanic before authorizing work.

Consumers must recognize that specialized efficiency in one area, such as tires, does not replace the broader diagnostic evaluation available at independent shops or dealerships.

About

Anna Petrova serves as a B2B Auto Parts Market Analyst at KZMALL, where she specializes in tracking demand trends and competitive dynamics within the global independent automotive aftermarket. Her daily work involves analyzing vast datasets on parts sourcing, fitment accuracy, and supply chain efficiency, making her uniquely qualified to interpret the recent Consumer Reports findings favoring independent repair shops. As KZMALL operates as a critical wholesale platform supplying over 50,000 SKUs to these exact independent facilities, Petrova directly observes how access to certified, single-source parts empowers local shops to compete effectively with dealerships. Her analysis bridges the gap between high-level consumer sentiment and the operational realities of parts procurement. By connecting survey data on customer satisfaction with the logistical advantages KZMALL provides to distributors and repairers, she offers actionable insights into why the independent repair sector continues to thrive through quality parts availability and simplified sourcing strategies.

Conclusion

Scaling a maintenance strategy across multiple vehicles exposes the fragility of fragmented service records. When drivers rely on specialized chains for commodity tasks while ignoring the diagnostic depth of generalists, they incur a hidden operational cost: the loss of longitudinal vehicle history. This data gap prevents mechanics from spotting subtle patterns that indicate systemic failure, forcing owners to pay premium rates for crisis management later. The statistical preference for independent shops is not merely about cost; it is a functional necessity for preserving asset value in an era of complex electronics.

Shop owners must proactively bridge the information gap to retain this expanding customer base. Within the next month, independent facilities should implement a standardized digital intake process that explicitly visualizes missing service history for every new customer. This transforms a potential liability into a consultative opportunity. Start this week by creating a simple one-page checklist that highlights exactly which diagnostic data points are missing from a vehicle's record compared to a full-service history. Presenting this visual gap to the driver demonstrates immediate value and justifies the shift from a transactional tire change to a thorough care partnership. This approach uses the inherent flexibility of the independent model to solve the specific anxiety of modern vehicle ownership.

Frequently Asked Questions

New vehicle complexity often forces owners to seek specialized dealer equipment for repairs. This technical barrier explains why 80% of drivers with new model year 2023 vehicles utilize dealerships instead of independent options.

Restricted access to proprietary vehicle data creates significant operational hurdles for many local repair facilities. Data access barriers complicate this choice, as 84% of independent shops view vehicle data restrictions as their top business issue.

Independent providers manage most aftermarket work but struggle with specific electronic calibration tasks. While independent shops perform roughly 75% of aftermarket work, complex electronic defects frequently fall outside their equipment scope requiring dealer intervention.

Owners of newer models heavily favor dealerships while older car owners prefer local shops. About 80% of drivers with a car from model year 2023 went to the dealership for their recent repair needs.

Many software tasks require direct manufacturer access that third-party scanners cannot replicate easily. Data access barriers complicate this choice, as 84% of independent shops view vehicle data restrictions as their top business issue today.