First Brands collapse: Fix your brake supply now

First Brands Group generated substantial revenue in 2024 before its collapse triggered immediate supply chain failure. This financial implosion forces Canadian jobbers to abandon passive distribution models and actively reconstruct their parts inventory strategies. The absence of debtor-in-possession financing means divisions like Brake Parts Inc. and Cardone Industries are dismantling without credible divestiture pathways, creating a void in daily-turn categories.

Distributors must now navigate the operational nightmare of removing entrenched brands like Raybestos and Centric Parts from their systems. This process demands rigorous validation of cross-references and complete renumbering of part numbers to maintain warranty processes. Counter staff require immediate retraining to handle these shifts while preventing long-term customer defection due to fill rate failures.

This bankruptcy accelerates market disruption and exposes the fragility of current supply chain mechanics. The analysis details the measurable ROI available to those who rationalize SKUs rather than reacting with urgency alone. Success depends on grounding decisions in SKU productivity analysis to secure category positioning against competitors ready to invest in aggressive conversion support.

The Role of First Brands Bankruptcy in Accelerating Market Disruption

First Brands Group Massive Debt Structure Collapse

First Brands Group failed because it could not service a massive debt load that included $4.6 billion in off-balance-sheet financing. This opaque model, mirroring supply chain finance vehicles previously associated with Greensill Capital, allowed the company to leverage its balance sheet beyond traditional limits. Off-balance-sheet instruments accounted for approximately 42% of total liabilities, a hidden structure that unraveled upon scrutiny. Distressed financing interest rates ranging between 12% and 18% in the current environment made securing debtor-in-possession funding impossible.

The result is the immediate wind-down of core assets within Brake Parts Inc. and Cardone Industries. Jobbers face urgent pressure to replace high-volume SKUs like Raybestos and Centric Parts. Hasty supplier selection risks future failures, yet delay invites customer defection. The hidden liability structure meant that standard due diligence missed the true scale of exposure until liquidation began. Distributors must now validate cross-references and retrain staff without the warranty support previously guaranteed by the parent entity. This structural reset forces a shift from single-source dependency to diversified inventory strategies grounded in SKU productivity analysis.

Canadian Jobber Impact on Raybestos and Cardone Lines

Operations for Canadian entities have ceased, forcing jobbers to replace Brake Parts Inc. and Cardone Industries lines without delay. This structural break removes Raybestos and Centric Parts from active supply, creating a vacuum in high-turn brake categories. Operators must now validate cross-references for thousands of SKUs to ensure correct fitment before listing alternative brands. Counter staff require retraining on new warranty protocols because legacy processes tied to the defunct entity no longer apply. Inventory exposure assessments must identify stranded stock that lacks manufacturer support. Inflation impacts parts distribution by compressing margins on these necessary replacements, forcing shops to absorb higher costs or pass them to consumers.

Inside the Supply Chain Mechanics of Parts Distribution Failure

Part Number Renumbering and Cross-Referencing Failure Modes

Legacy cross-reference tables fracture when bankruptcy liquidation forces immediate part number renumbering across deprecated SKUs. When First Brands Group permanently closed its Hebron facility, the resulting data void rendered thousands of valid inventory items invisible to jobber management systems. This mechanism fails because legacy databases rely on static manufacturer identifiers that do not update dynamically during asset sales.

- Original OEM numbers lose linkage to active supplier catalogs.

- Warehouse management systems flag in-stock items as obsolete.

- Counter staff cannot validate fitment without updated interchange data.

| Failure Mode | Technical Consequence | Operator Impact |

|---|---|---|

| Static Lookup | Valid stock appears unavailable | Lost sales opportunities |

| Missing Metadata | Warranty validation fails | Increased return rates |

| Delayed Updates | Catalog synchronization lag | Extended lead times |

Manual verification cannot scale to match the volume of affected SKUs during rapid liquidation events. Unlike standard discontinuations, bankruptcy-driven changes lack coordinated data migration, leaving jobbers to reconstruct fitment matrices blindly. Operators must prioritize SKU validation for high-turn categories before attempting broad catalog updates. Without verified interchange files, selling remaining inventory carries significant liability risk for incorrect applications. Products and Brands advises operators to suspend automated reordering on affected lines until new supplier data integrates fully. The structural reset demands a shift from reactive substitution to proactive data auditing.

Resolving Inventory Mismatches After Brand Discontinuation

Jobbers fix inventory mismatches after brand discontinuation by executing a strict three-step validation workflow against active supplier databases. The sudden absence of Brake Parts Inc. SKUs forces immediate cross-referencing to prevent fitment errors in high-turn brake categories. Operators must map legacy part numbers to new manufacturer identifiers before listing alternatives for shop customers.

- Audit current stock for stranded Raybestos and Cardone items lacking warranty support.

- Validate fitment data using updated electronic catalogs from surviving strategic buyers.

- Retrain counter staff on new return protocols for discontinued lines.

| Legacy Status | Action Required | Risk Factor |

|---|---|---|

| Active SKU | Map to new vendor | Low |

| Discontinued | Quarantine stock | High |

| Obsolete | Liquidate locally | Medium |

The Canadian jobber market 2026 faces unique pressure as trade policy uncertainty complicates sourcing replacements from integrated North American networks. Even marginal adjustments can ripple through pricing structures and supplier availability for distributors reliant on cross-border flows. A critical tension exists between rapid stock replenishment and accurate data migration; rushing the process often leads to incorrect part number assignments that trigger costly returns. Unlike standard supplier switches, this scenario involves validating stock against databases of entities acquiring assets through liquidation rather than organic growth. The limitation here is temporal: legacy database links break permanently once the original manufacturer ceases updates, creating a finite window for accurate cross-reference validation before data integrity degrades.

Labor Market Volatility and Deferred Repair Risks

A net loss of 25,000 jobs alongside an unemployment rate edging to 6.5 percent directly constrains household disposable income for non-necessary automotive maintenance. When consumers face tightened budgets, they frequently postpone deferred repairs on aging vehicles rather than risking immediate mechanical failure. This behavioral shift reduces order frequency for jobbers holding stranded inventory from dissolved supply lines. The Canadian jobber market 2026 now faces a dual pressure: replacing discontinued product lines while managing slower receivables from struggling repair shops.

| Factor | Pre-Disruption Model | Post-Disruption Reality |

|---|---|---|

| Revenue Source | Steady turnover of brake parts | Volatile, repair-delay dependent |

| Credit Risk | Low default rates | Elevated shop insolvency risk |

| Inventory Strategy | Just-in-time restocking | Conservative cash preservation |

Older vehicle Parc trends suggest sustained long-term demand, yet short-term cash flow remains the primary bottleneck for small operators. Shops may delay authorizing work even when parts are available, creating a lag between inventory availability and actual sales realization. Jobbers must tighten credit terms to avoid compounding losses from both bad debt and obsolete stock. Failure to adjust credit management protocols risks turning liquid inventory into written-off assets. The operational focus shifts from maximizing fill rates to preserving capital liquidity during this contraction.

Measurable ROI from Diversifying Suppliers and Rationalizing SKUs

Defining SKU Productivity Analysis Amid Line Instability

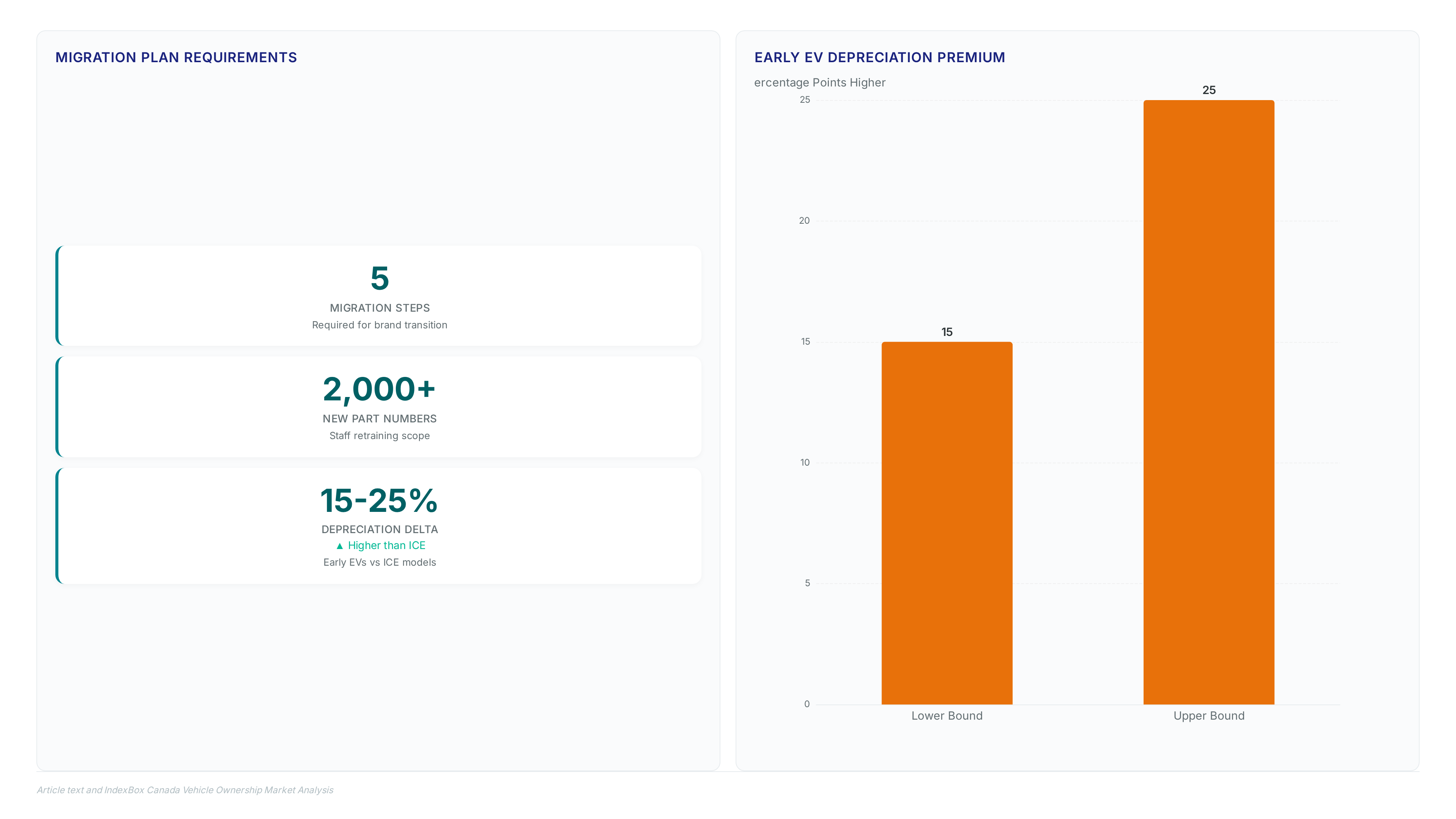

SKU productivity analysis measures profit contribution per distinct part number rather than total category revenue, a vital distinction when Raybestos lines face sudden discontinuation. This metric isolates underperforming assets by comparing holding costs against actual turnover rates, forcing jobbers to identify stranded inventory before capital becomes unrecoverable. The Canadian automotive aftermarket generated between CAD 25 billion and CAD 30 billion in 2026, yet this aggregate volume masks severe fragmentation risks within specific brake and remanufactured sub-sectors. Operators must now weight turnover velocity heavily because supply continuity guarantees future shop loyalty.

A critical tension exists between maintaining broad catalog depth for customer convenience and the urgent need to rationalize inventory exposure across unstable supply chains. Effective analysis requires discarding legacy suppliers who cannot guarantee fill rate performance regardless of past relationship value. Durability in this context will come from using data to purge non-viable SKUs immediately.

Executing Vendor Diversification for Brake Part Suppliers

Jobbers must replace stranded Brake Parts Inc. inventory by activating pre-qualified secondary vendors before liquidity crises halt shipments. Relying on a single source for high-turn brake categories creates a fragile supply chain that collapses when primary suppliers face insolvency. The sudden facility closure in Hebron demonstrates how quickly asset wind-downs sever distribution lines.

| Risk Factor | Single-Source Dependency | Diversified Supply Chain |

|---|---|---|

| Fill Rate Stability | Collapses during vendor distress | Maintained via alternate channels |

| Pricing Use | Non-existent during shortages | Preserved through competition |

| Warranty Support | Unavailable post-liquidation | Backed by solvent partners |

However, switching suppliers introduces fitment validation costs that erode initial savings. Technicians require retraining on new part numbering schemes to avoid costly installation errors. This operational friction often delays full adoption despite clear long-term benefits. The multimillion-dollar tariff claim against the parent company suggests previous pricing relied on unsustainable duty avoidance, meaning replacement parts may carry higher baseline costs. Distributors must adjust margin expectations accordingly. Products and Brands offers the necessary data tools to rationalize SKU productivity across these new vendor relationships. Ignoring this structural reset invites permanent customer defection to competitors with stable stock. The market no longer tolerates inventory gaps in necessary repair categories.

Checklist for Rationalizing SKUs During Market Normalization

Jobbers must validate credit exposure against technician support needs before committing capital to new brake lines. The average age of vehicles in Canada reached 13–14 years in 2026, driving steady demand for replacement parts despite broader economic caution. This aging fleet creates a specific window where targeted SKU rationalization yields immediate liquidity without sacrificing fill rates.

- Audit inventory for stranded assets lacking active warranty backing from original manufacturers.

- Cross-reference part numbers against current shop repair orders to identify true turnover velocity.

- Schedule technician training sessions only when demand for specific system integrations exceeds internal knowledge thresholds.

- Diversify supplier base to prevent single-point failures in critical categories like remanufactured components.

| Action | Trigger Condition | Operational Impact |

|---|---|---|

| Credit Review | Unpaid invoices exceed 30 days | Prevents bad debt accumulation |

| Training Investment | New platform adoption | Reduces counter error rates |

| SKU Culling | Zero sales in 90 days | Frees working capital |

Investing in technician training makes sense only when the underlying vehicle parc requires complex diagnostics that generic parts cannot address. Failure to align inventory strategy with actual repair shop capabilities results in dead stock rather than strategic depth.

Migrating to Resilient Distribution Models in Five Steps

Defining Operational Recalibration for Brake Categories

Operational recalibration demands immediate substitution of single-source dependencies with diversified supply chains following the First Brands Group collapse. Standard inventory models fail when Brake Parts Inc. assets liquidate because catalog cross-references vanish quicker than replacement lines activate. This disruption forces a shift from passive replenishment to active vendor diversification across multiple manufacturers.

- Audit existing stock for Raybestos and Centric Parts to quantify exposure before value evaporates.

- Validate alternative supplier credentials to guarantee warranty support matches original equipment standards.

- Reconfigure purchasing algorithms to prioritize fill-rate stability over marginal unit-cost savings.

The market correction reveals that private equity consolidation often masks underlying fragility in distribution networks distributionstrategy.com. However, rushing into new contracts without credit vigilance exposes jobbers to secondary insolvency risks. The limitation here is time; securing diverse vendors often conflicts with the urgency required to restock high-turn brake categories. Consequently, operators must balance speed against due diligence to avoid compounding supply chain errors. This strategic pivot ensures long-term viability where previous reliance on broad-line distributors proved catastrophic.

Retraining Counter Staff on Raybestos and Cardone Replacements

Immediate retraining starts by freezing all Raybestos cross-references in the catalog system to prevent false availability claims.

- Map legacy part numbers from Brake Parts Inc. and Cardone Industries to verified alternative SKUs before updating point-of-sale databases.

- Deploy printed conversion charts at every counter station to guide staff through manual lookups during the digital transition.

- Role-play objection handling scenarios where technicians question the warranty backing of new replacement brands.

Counter staff must shift from passive order-taking to active inventory substitution because the liquidation of core assets eliminates future stock replenishment for discontinued lines.

Execute a hard freeze on Brake Parts Inc. cross-references to prevent false availability claims during the asset wind-down.

- Audit physical stock for Raybestos and Centric Parts to quantify exposure before liquidation value evaporates completely.

- Validate alternative supplier credentials against current shop repair orders to guarantee warranty support matches original equipment standards.

- Reconfigure purchasing algorithms to flag single-source dependencies that risk fill-rate collapse during inventory liquidation.

- Update point-of-sale databases with verified part numbers from diversified vendors to maintain counter accuracy.

- Deploy printed conversion charts at every station to guide staff through manual lookups during the digital transition.

| Validation Step | Legacy Dependency Risk | Diversified Strategy Outcome |

|---|---|---|

| Cross-Reference Check | False positive availability | Verified substitution paths |

| Warranty Verification | Unbacked returns | Protected margin integrity |

| Stock Audit | Stranded capital | Liquidated exposure |

The hidden tension lies between maintaining fill rate stability and avoiding capital commitment to stranded SKUs lacking future supply. Operators delaying this validation face a narrower window for recovery as trade uncertainty weighs on the Canadian automotive industry through 2026. Products and Brands recommends immediate execution of these steps to secure daily-turn categories.

About

Mark Phillips serves as Editor of Aftermarket Intel at KZMALL, where he daily analyzes global distribution shifts and competitive dynamics within the independent automotive aftermarket. His extensive background tracking substantial distributor movements and e-commerce evolution uniquely positions him to dissect the fallout from the First Brands Group bankruptcy. As First Brands' collapse creates immediate product-line instability, Phillips uses his frontline access to wholesale data to explain how jobbers must pivot from passive observation to active supply chain management. His work at KZMALL, a platform built on standardized fitment data and single-source reliability, directly informs his perspective on mitigating disruption through diversified sourcing. By connecting macroeconomic moderation with acute industry shocks, Phillips provides critical insights for distributors navigating this structural reset. His analysis bridges the gap between high-level market trends and the practical realities faced by warehouses and retailers seeking stability amid uncertainty.

Conclusion

The collapse reveals that off-balance-sheet financing creates a fatal fragility when interest rates climb into the double digits. While an aging vehicle fleet drives steady demand for replacement parts, distributors cannot rely on suppliers using hidden debt instruments to fund inventory. The operational cost of this failure is lost stock but the erosion of counter credibility when promised parts do not exist. Shops must treat supplier financial health as a critical component of their own supply chain security.

Distributors should immediately halt any new credit exposure to vendors with opaque capital structures before the next fiscal quarter begins. This is not about predicting market crashes but recognizing that high-cost debt loads make suppliers unreliable partners during economic shifts. You cannot build a stable inventory strategy on a foundation of 12% to 18% interest obligations that prioritize debt service over product availability.

Start by auditing your top five supplier relationships this week to identify any reliance on single-source components lacking verified backup options. Cross-reference your current stock of legacy brands against active purchase orders to quantify exposure before liquidation events force price volatility. Secure your margin integrity by diversifying sources now rather than reacting to shortages later.

Frequently Asked Questions

The failure resulted from an billions debt load including hidden financing. This $4.6 billion in off-balance-sheet instruments created opaque liabilities that prevented rescue funding and forced immediate asset wind-downs for distributors.

Lenders demanded interest rates between 12% and 18% due to high risk. These prohibitive costs made securing debtor-in-possession funding impossible, forcing the dismantling of core divisions like Brake Parts Inc. without credible divestiture pathways.

Off-balance-sheet instruments accounted for approximately 42% of total liabilities. This hidden structure meant standard due diligence missed the true exposure scale, leaving jobbers to suddenly validate cross-references for thousands of unsupported SKUs.

The group generated over billions in revenue prior to collapse. This massive volume means the sudden supply chain failure creates immediate voids in daily-turn categories that require urgent supplier diversification strategies.

A specific claim of approximately millions for alleged tariff underpayment strained resources. While large, this amount was secondary to the billions debt structure that ultimately made restructuring financially unviable for the entity.