Service programs stop EV obsolescence now

The Canadian aftermarket's survival hinges on one immediate action: adopting structured EV service programs like NAPA NexDrive.

Electrification isn't a distant threat; it is the current reality where capability has replaced mechanical intuition as the baseline for competition. Yves Racette of NexDrive puts it bluntly: independent shops must build high-voltage diagnostic capacity now or face total exclusion from future revenue streams. This isn't about adding a new service line; it's about avoiding obsolescence. NAPA NexDrive combines technician upskilling with rigid high-voltage handling protocols to solve this. The path forward requires independent operators to implement EV certification immediately, capturing value in a market where ADAS-equipped vehicles already dominate the parc.

S&P Global projects ADAS adoption will hit 69% of North American vehicles by 2035. The window to establish technical credibility is slamming shut. Generic repair is dead. The future belongs to networks that standardize software-driven troubleshooting and battery diagnostics today.

The Strategic Role of Structured EV Service Programs in Aftermarket Survival

NAPA NexDrive: Defining Structured EV Service Programs

NAPA NexDrive fuses advanced technician training, specialized tooling, and standardized service protocols into a single operational framework. Launched in Canada during late 2023, the program addresses high-voltage safety through rigorous certification rather than relying on general mechanical familiarity. Yves Racette, director of NexDrive program development, insists that independent shops must build capability immediately as the transition accelerates. Operational success now demands access to OEM maintenance data to preserve manufacturer warranties while handling battery diagnostics. During the initial rollout year, approximately 150 NAPA Auto Parts stores were expected to obtain High Voltage certification. This specific credentialing separates participating locations from competitors lacking electric drivetrain authorization. NAPA Auto Parts uses this structure to maintain relevance against large-scale rivals. Capital intensity creates a hard barrier; shops unable to fund specialized tooling face exclusion from fleet contracts requiring certified partners. Without this structured approach, independent operators risk losing service revenue to dealerships that control proprietary software access. Capability now dictates survival more than geographic proximity.

Applying Standardized Protocols for High-Voltage Battery Diagnostics

Rigid safety interlocks and software-set workflows have replaced traditional mechanical intuition. High-voltage system handling requires software-driven troubleshooting to interpret battery management system logs before physical contact occurs, a stark contrast to traditional repair which relied on physical wear indicators. The Canadian automotive aftermarket, valued between a substantial amount and an even larger sum USD, faces immediate pressure to adopt these methods as fleet electrification accelerates. Operators asking whether to invest in certification now confront a binary outcome: certified integration or exclusion from future service contracts. There is no middle ground.

Inside the Mechanics of Charging Infrastructure and Fleet Ecosystems

Charging networks now function as the primary engagement layer, pushing traditional repair shops to the periphery. A dominant theme at the recent expo highlighted charging infrastructure, specifically energy management systems, over the vehicles themselves. This structural shift means the charging experience replaces the repair bay as the main point of contact. Independent operators risk obsolescence if they ignore this transition, as charging networks increasingly dictate service access. Fleet electrification accelerates this shift through centralized decision-making and uptime mandates. Municipal fleets and last-mile delivery providers prioritize operational reliability over transactional repairs. The federal nominal fee structure supports this, but the operational burden falls on the service provider.

Fleet Electrification Drivers: Municipal Fleets and Last-Mile Delivery Operators

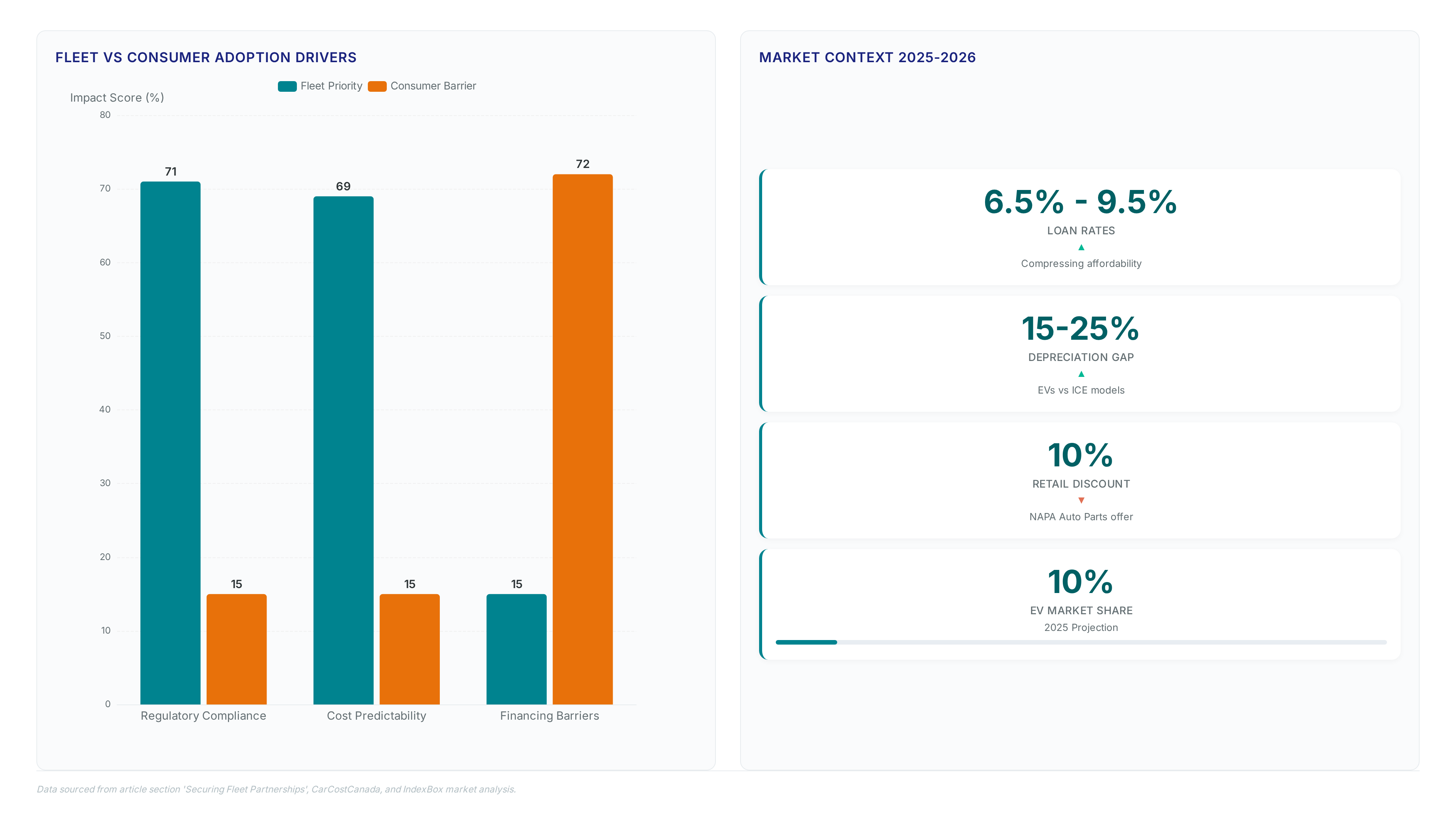

Municipal mandates and last-mile delivery logistics drive immediate EV adoption through centralized procurement rather than consumer preference. Regulatory pressure forces fleet operators to prioritize uptime guarantees over transactional repair models, fundamentally altering service requirements. This financial structure specifically targets commercial scalability, allowing fleet managers to offset initial capital expenditures while adhering to strict decarbonization timelines. Retail service models fail in this sector because fleet operations demand predictive maintenance schedules aligned with depot charging cycles. Independent shops must integrate with energy management systems to remain relevant as charging infrastructure becomes the primary customer touchpoint. Financing costs remain elevated, compressing affordability for smaller operators despite federal aid. Shops relying on NAPA PROLink Architecture face a hard constraint: technical certification. Without high-voltage training, independent providers cannot bid on municipal contracts. Failure to align with structured programs like NAPA NexDrive guarantees exclusion.

Residual Value Uncertainty from Early-Generation BEV Depreciation Rates

Early-generation battery-electric models suffer 15-25% higher depreciation than internal combustion equivalents, creating immediate residual value uncertainty for service partners delaying capability investment. This financial erosion signals that waiting for volume before adapting is a high-risk strategy rather than a conservative hold. Data indicates early-generation battery-electric models depreciate rapidly. Consequently, shops lacking technician readiness for complex EV ecosystems lose access to these distressed assets entirely. The constraint lies in the narrow window for integration; once depreciation stabilizes, legacy operators may find themselves excluded from the secondary service market. Networks must integrate into EV ecosystems now to capture fleet electrification opportunities before asset values reset. Operators ignoring this shift face disintermediation as certified partners secure long-term contracts with depreciating fleets seeking cost-effective maintenance. The strategic danger is clear: capacity built after the market correction arrives will yield diminishing returns on investment.

Implementing EV Certification and Charging Services in Independent Shops

NAPA NexDrive Components for Independent Shop Readiness

NAPA NexDrive readiness demands immediate enrollment in advanced technician training, acquisition of specialized tooling, and strict adherence to standardized service protocols. Independent shops must execute these four implementation steps to safely handle high-voltage systems.

- Submit applications for NAPA High Voltage certification to access the necessary supply chain adjustments.

- Deploy OEM-specific diagnostic software to maintain manufacturer warranty compliance on hybrid platforms.

- Install insulated tooling sets rated for voltages exceeding 600 volts.

- Integrate charging network troubleshooting into daily service workflows.

The NexDrive program moves fast. By late 2023, approximately 150 locations obtained certification, signaling that NAPA Auto Parts prioritizes verified safety over general mechanical history. Exclusivity defines the cost of this specialization. Shops failing to publish their certified status to the network remain invisible to fleet contracts demanding audited safety records. Standardized service protocols now function as the primary gatekeeper for revenue, replacing traditional reputation metrics. A shortage of certified instructors creates a bottleneck where demand for training outpaces available course slots. This constraint forces operators to schedule certification cycles quarterly rather than annually to maintain workforce readiness.

Expanding Into Charging Installation and Site Management Services

Repositioning as necessary local partners requires targeting commercial and multi-residential applications where infrastructure demands ongoing maintenance.

- Audit site electrical capacity against projected charging networks load requirements.

- Deploy energy management software to peak-shave demand charges.

- Establish 24/7 remote monitoring for uptime guarantees.

- Integrate billing systems with fleet card providers.

A tension exists between mechanical repair revenue and service fee stability within the site management role. Independent operators gain a foothold in the VinFast partnership Charging downtime directly halts fleet operations, making reliability the primary metric rather than repair speed. This shift requires shops to master utility interconnection protocols alongside high-voltage safety. Failure to integrate energy management systems risks stranding assets when utilities curtail power during peak events. The operational cost of idle chargers exceeds mechanical bay downtime, forcing a strategic pivot toward software-driven service contracts.

Implementation: Revenue Loss Risks From Ignoring the EV Service Transition

Mechanical repair focus reduces customer touchpoints as the charging experience replaces the service bay as the primary engagement layer.

- Enroll technicians in NexDrive.

- Deploy high-voltage tooling rated for specific battery architectures to capture early-adopter fleets.

- Integrate site management protocols to monetize energy uptime rather than waiting for mechanical failure.

The limitation is stark: ADAS penetration reaches 71% of vehicles by 2035, yet many independents lack software diagnostic access. Operators ignoring this shift cede the customer relationship to chargers and OEMs, leaving only low-margin commodity work. Delay results in exclusion from the retailers' cooperative networks that fleets increasingly mandate for service contracts. Market data from 09/19/2025 highlights the urgency, noting that 71% of new vehicles will rely on software diagnostics. By 2035, the gap between certified and non-certified shops will determine survival. The window for adaptation closes rapidly as 2025 approaches.

Securing Fleet Partnerships to Solve Demand Gaps in EV Servicing

Application: Fleet Electrification Drivers: Municipal and Last-Mile Operators

Municipal fleets and last-mile delivery operators drive near-term EV demand through centralized decision-making structures distinct from consumer adoption curves. These segments prioritize regulatory compliance and cost predictability over the financing barriers compressing affordability for private buyers, as elevated financing costs Unlike retail customers influenced by transaction incentives, fleet managers execute bulk transitions based on operational lifecycle calculations. This centralization allows independent shops to secure long-term service agreements by aligning with NAPA NexDrive protocols that guarantee standardized high-voltage handling. The mechanism relies on shops demonstrating capacity for uptime-critical maintenance rather than opportunistic repairs.

Independent operators should align with NAPA NexDrive to validate technical competence for these contracts, as seen in the September 2025 VinFast partnership announcement. The mechanism relies on converting federal purchase subsidies into long-term service agreements rather than one-time repairs. However, the strategy faces friction because the federal cap does not apply to Canadian-made vehicles, creating pricing distortions that complicate TCO calculations for mixed fleets. New vehicle loan rates ranging from moderate to elevated levels compress affordability for smaller commercial providers, forcing shops to offer flexible payment terms for maintenance packages. The implication for network engineers and shop owners is clear: capturing fleet demand requires integrating charging infrastructure support into standard service workflows immediately. Waiting for retail volume to mature while ignoring these federally subsidized fleet pilots risks permanent exclusion from the commercial supply chain. Products and Brands recommends using these specific incentive structures to lock in multi-year maintenance contracts before competitors secure the limited pool of qualified service providers.

Validating Shop Readiness for Centralized Fleet Service Contracts

Fleet contracts demand certified high-voltage tooling to satisfy strict uptime mandates that retail customers rarely enforce. Independent operators must prove technical competency through structured curricula like the NexDrive Without such credentials, shops cannot validate safety protocols required by municipal procurement officers. The limitation remains that certification alone fails to address the capital intensity of depot upgrades. Financing costs constrain small operators, yet fleet partners require guaranteed operational reliability regardless of a shop's cash flow.

| Requirement | Fleet Mandate | Independent Gap |

|---|---|---|

| Technician Credentials | OEM-aligned certification | Generic mechanical experience |

| Service Scope | 24/7 uptime guarantees | Standard business hours |

| Infrastructure | High-voltage safety zones | Legacy bay configurations |

Shops ignoring this capability gap face exclusion as the industry shifts toward centralized decision-making. A tension exists between maintaining legacy mechanical revenue and investing in unproven EV service lines. Operators must audit electrical capacity before signing agreements to avoid default penalties. The retailers' cooperative model offers a path to share these infrastructure costs across networks. Failure to integrate these standards results in lost relevance within the commercial sector.

About

Ray Donnelly, Master Automotive Technician and Aftermarket Parts Authority at KZMALL Auto Parts, brings over two decades of hands-on repair and distribution expertise to the critical discussion on structured EV service programs. Having transitioned from running an independent shop to leading technical content strategy, Ray understands the precise operational shifts required as the industry moves from traditional disruption to strategic electrification. His daily work involves analyzing fitment data and service part requirements across 50,000+ SKUs, directly connecting him to the evolving needs of fleets and service providers adapting to EV maintenance. At KZMALL, a global B2B platform specializing in standardized aftermarket solutions, Ray uses his ASE Master Certification to guide independent shops through this transition. His insights bridge the gap between high-level expo trends and the practical reality of stocking the right components for next-generation vehicles, ensuring service providers remain competitive as revenue mixes evolve in the Canadian market.

Conclusion

The real fracture point for independent shops isn't technical ability; it's the cash flow mismatch between immediate infrastructure spend and delayed fleet reimbursement cycles. While high-voltage certification gets you in the door, the operational reality of 24/7 uptime guarantees creates a liability trap for operators running on legacy margin structures. You cannot sustain commercial EV contracts with retail-style working capital. The window to negotiate shared-infrastructure deals within retailer cooperatives closes within 18 months as substantial fleets finalize exclusive provider lists. Do not attempt to bridge this gap with high-interest vehicle loans; instead, structure proposals that explicitly separate tooling amortization from labor rates.

Start by auditing your electrical panel capacity and local utility demand charges this week before evaluating any service contract. Many shops will sign agreements only to discover their upgrade costs exceed three years of projected profit, turning a "lucrative" deal into a financial anchor. Prioritize partners who offer lease-to-own equipment models rather than those demanding full capital expenditure upfront. This specific financial vetting protects your solvency improved than any mechanical credential. Secure your energy infrastructure math first, then pursue the certification.

Frequently Asked Questions

Uncertified shops face exclusion from future fleet and consumer revenue streams. This risk grows as the vehicle parc reaches 27 million units by 2026, making certified integration essential for survival.

NAPA NexDrive combines advanced training, specialized tooling, and standardized protocols for safety. This approach addresses the $25 billion Canadian aftermarket value by ensuring shops can handle high-voltage diagnostics effectively.

EV diagnostics require software-driven troubleshooting to interpret battery logs before physical contact occurs. This shift is critical as ADAS adoption hits 69% of North American vehicles by 2035.

The Canadian automotive aftermarket is valued between 17.3 billion and 22.4 billion USD. This significant sector faces immediate pressure to adopt standardized high-voltage handling protocols as fleet electrification accelerates rapidly.

Charging infrastructure replaces traditional repair bays as the primary customer engagement point. Shops must expand into charging services to avoid losing touchpoints in this evolving ecosystem dominated by energy management.