Aftermarket Canada: 2026 new car sales drop 4.3%

New vehicle sales in Canada are projected to drop 4.3% in 2026. For the automotive aftermarket, this contraction signals a counter-cyclical surge. An aging fleet demands attention.

Global volatility creates noise, but the core thesis is simple: economic stagnation and deferred maintenance create a measurable tailwind for independent repair shops. As TD Economics forecasts a contraction to 1.9 million new units, consumers extend the life of existing vehicles. Market anxiety translates directly into repair demand. This shift moves consumer spending from discretionary upgrades to critical safety repairs. In an environment where Statistics Canada notes population declines and rising unemployment, shop stability depends on operational excellence, not economic luck.

The Role of Macroeconomic Volatility in Shaping Aftermarket Demand

Defining Core Inflation and CPI Divergence in 2026

Headline CPI fell to 1.8 per cent in February 2026. Core inflation dropped to four-year lows. These figures mask immediate energy risks. The divergence separates temporary price shocks from persistent monetary pressure. Statistics Canada reported the February Consumer Price Index (CPI) at 1.8 per cent year-over-year, down from 2.3 per cent in January. This metric excludes volatile food and energy components that drive shop overhead. The Bank of Canada held its policy rate at 2.25% citing softer domestic growth, creating a complex trade-off between curbing prices and supporting employment. Low core readings encourage rate cuts, but surging oil prices from geopolitical conflict threaten to reignite headline inflation before policy adjusts.

Distribution channels shift alongside ownership patterns. Independent retailers face competition from e-commerce, which now captures nearly 25 per cent of the independent segment sales. Physical stores must optimize inventory turnover to compete with digital agility. Early-generation electric models introduce volatility through accelerated depreciation, creating uncertainty for residual values compared to internal combustion engines. The aftermarket durability stems from forced retention. Consumers cannot afford new units, so they invest in preserving current assets. This flexibility insulates repair demand from the volatility seen in primary manufacturing sales. Shop owners benefit from a captive audience unable to exit the market due to prohibitive replacement costs.

Volatility Risks: Labor Losses and Energy Price Shocks

Population figures contracted by 55,025 people in early 2026. This tightens the labor pool available for aftermarket services. Demographic shrinkage coincides with a softening domestic market where job losses directly erode consumer spending power for non-necessary repairs. Shops face a dual threat: fewer potential customers and reduced disposable income per capita. Crude oil prices surged from $70 to over a hundred dollars per barrel following Middle East conflicts, creating immediate energy price shocks. Such volatility forces operators to absorb rising overhead before passing costs to clients. Reliance on global supply chains exposes local shops to petrochemical shortages derived from crude disruptions. The automotive aftermarket picture remains detailed but favourable compared to other sectors. Operators must optimize internal processes since external macro conditions dictate limited control over fuel or demographics. Deferred maintenance will eventually surface as costly failures, driving demand despite current hesitancy.

Inside the Mechanics of Deferred Maintenance and Labor Market Shifts

Deferred Maintenance Mechanics and Vehicle Age Impact

The fleet now averages 13–14 years. This aging model forces reliance on older components. Skipped oil changes or ignored belt inspections compound into catastrophic failures rather than routine service.

The definition of proven labor rate shifts in this environment. It moves from a simple revenue metric to a survival indicator. Operators must calculate this figure by dividing total gross profit by billed hours. Pricing must cover the increased diagnostic time required for aged vehicles with modified or worn systems. High financing costs, with loan rates reaching 9.5%, discourage new purchases and keep defective units on the road longer.

| Factor | Impact on Aged Fleet | Operational Consequence |

|---|---|---|

| Component Fatigue | Exponential failure risk | Higher warranty claim rejection |

| Financing Costs | Reduced turnover | Extended repair intervals |

| Labor Complexity | Increased diagnostic time | Lower proven labor rate |

A softening labor market creates a counter-intuitive tension. Shops struggle to staff despite rising repair volumes. Consumer demand for fixes grows due to the inability to buy new, yet the pool of qualified technicians shrinks as economic uncertainty drives workforce exits. Capacity is the limitation; shops cannot capture additional revenue without the human capital to perform the work. Owners must prioritize retention strategies over expansion to prevent bottlenecks from eroding margins.

Labor Shortages Disrupting Shop Operations and Repair Orders

The loss of 84,000 jobs in February directly reduced the customer base capable of funding non-necessary vehicle repairs. This contraction suppresses discretionary spending. Shop owners contend with declining repair orders despite an aging national fleet. Rising unemployment creates a specific bottleneck where consumers delay maintenance until catastrophic failure occurs, altering the typical service cadence shops rely on for steady revenue.

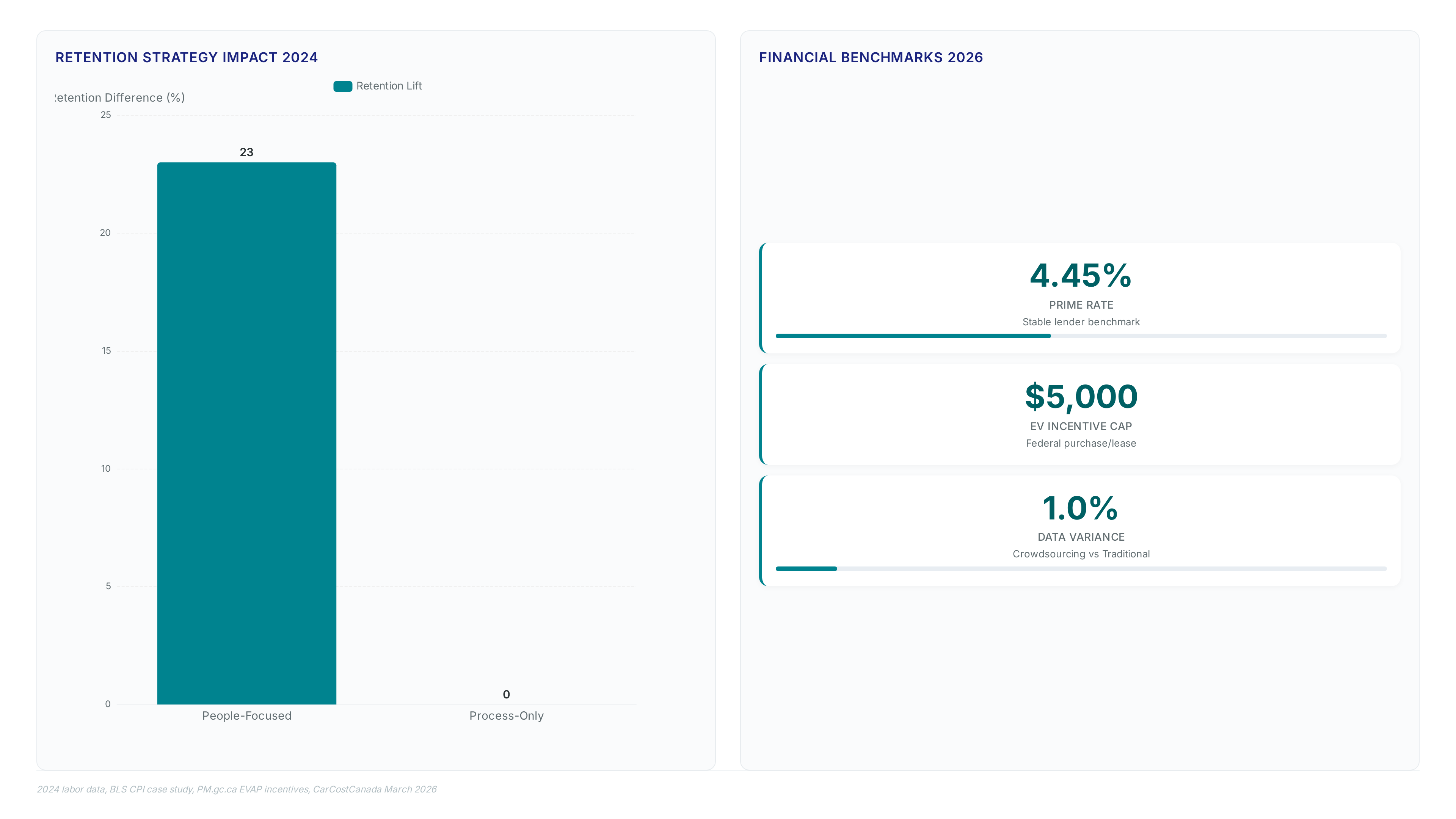

Consumer lenders' prime rate remained stable at approximately 4.45 per cent, while rates from 5 per cent to 9.5 per cent continue to bar entry for many buyers. This financing barrier keeps older cars on the road, but the owners of these vehicles often lack the liquidity for proactive care. The result is a shift from scheduled maintenance to emergency breakdown response, straining shop scheduling and parts inventory management.

| Factor | Impact on Shop Operations |

|---|---|

| Job Losses | Reduced volume of non-critical repair orders |

| High Loan Rates | Extended vehicle life, delayed maintenance cycles |

| Deferred Repairs | Increased complexity and diagnostic time per job |

Cross-border tariffs and stalled financing conditions reduce new car purchases, theoretically increasing the total addressable market for repairs over time. However, the immediate reality for operators is a cash-flow crisis among their clientele. Shops must adapt their service models to address this liquidity constraint, perhaps by prioritizing necessary safety repairs over upselling. Without adjusting to this labor market softening, fixed overhead costs will quickly outpace the revenue from fewer, more complex jobs. The structural shift toward older vehicles ensures long-term demand, but surviving the current dip requires managing the gap between necessary repairs and available consumer funds.

Parts Supply Disruption and Parts-to-Labor Ratio Instability

Brent crude touching a record high creates immediate polymeric feedstock shortages. This skews the parts-to-labor ratio toward inventory bloat. Supply chain fractures in the Strait of Hormuz alter petrochemical outputs, forcing shops to hold expensive stock while waiting for components. This imbalance inflates working capital requirements precisely when liquidity is scarce. The mechanical risk manifests as stalled bays where technicians lack specific automatic tire inflation systems or trim pieces, driving labor efficiency down despite high demand.

| Factor | Supply Constrained | Labor Constrained |

|---|---|---|

| Primary Bottleneck | Polymer feedstock availability | Skilled technician count |

| Revenue Impact | Delayed RO closure | Underutilized bay hours |

| Inventory Risk | High obsolescence cost | Minimal carry cost |

| Mitigation | Diversified vendor lists | Cross-training programs |

Operators face a divergence where traditional metrics fail; high parts sales no longer guarantee profitability if turnover slows. Online channels present a critical tension between maintaining deep inventory buffers and preserving cash flow against rising borrowing costs near 4.45 per cent. Shops over-indexing on parts stockpiles risk insolvency if the labor market softens. The cost of misalignment is measurable: stalled repairs generate zero revenue while fixed overheads accumulate daily.

Measurable ROI from Doubling Down on People and Process

Defining the Internal Control Variable in Unpredictable Markets

External volatility dictates market noise. The winning strategy isolates Process and People as the only actionable variables. When macro indicators fracture, operators controlling internal workflow efficiency outperform peers reacting to energy price shocks. Shops ignoring this shift miss revenue trapped in complex battery thermal management repairs.

Financial stability requires tracking the parts-to-labor ratio against stable lender benchmarks like the 4.45 per cent prime rate. A rigid focus on external inflation ignores how internal communication gaps erode margins quicker than rising crude costs.

Operators should adopt a two-pronged internal audit:

- Measure intake efficiency by tracking thorough inspection presentation rates versus complaint-only write-ups.

- Calculate proven labor rate weekly to identify pricing leaks before they compound.

Federal incentives up to $5,000 for eligible EVs alter consumer purchase behavior, yet the repairable fleet continues aging. Controlling the controllable means optimizing the four walls while external cycles turn.

Optimizing Intake Efficiency and Hours Per Repair Order

Service advisor workflow dictates revenue capture. Many shops still record only customer complaints instead of performing thorough inspections. This omission leaves money on the table as traditional retailers compete against e-commerce sectors accounting for up to a quarter of independent sales. Operators must track hours per repair order alongside the proven labour rate to identify diagnostic bottlenecks. A structural shift toward older vehicles drives sustained demand, with the average age of vehicles in Canada reaching 13–14.

| Metric | Operational Target | Risk of Neglect |

|---|---|---|

| Intake Comprehensiveness | thorough visual inspection | Missed upsell opportunities |

| Hours Per RO | >1.8 billed hours | Underutilized technician time |

| Parts-to-Labour | Balanced ratio | Inventory bloat or stockouts |

Retention remains cheaper than recruitment, especially when the industry directly employed more than 125,000 people and contributed a substantial amount to GDP. Improving intake speed often conflicts with inspection depth; rushing the write-up reduces the hours per repair order by missing necessary repairs. The cost of this trade-off is measurable in lost gross profit per vehicle. Shops implementing rigid Process controls see immediate gains in throughput without adding bays.

Digital transformation is no longer optional as competitors deploy automated systems that generated significant revenue increases in other retail sectors. Fix Network operators use these data points to refine their Speedy Auto Service intake protocols. The limitation lies in technician training; without clear communication standards, new metrics confuse rather than clarify. People must understand that thorough inspections protect the customer from future catastrophic failure. Controlling these internal variables isolates the business from external economic noise.

Retention Economics Versus Recruitment Costs in Technician Shortages

Retaining existing staff costs significantly less than replacing departed technicians. This financial reality defines shop survival during labor volatility. The industry directly employs more than 125,000 people. High turnover forces operators to rely on crowdsourced data for wage benchmarks, which can deviate by less than 1.0% from traditional surveys but lacks the nuance of local shop culture dynamics. Shops that fail to support ownership risk losing talent to competitors who understand that Process optimization depends on experienced hands. A UK case study showed automated systems yielding £500,000 in revenue, yet human capital automation via culture yields higher margins in service bays. Culture cannot be purchased instantly like inventory. Operators must anchor their teams with clear communication paths to prevent talent leakage to larger chains. Winning this people war ensures the business captures demand from the aging fleet without the drag of constant retraining cycles.

Migrating to a Resilient Operation with Workflow and Inventory Protocols

Implementation: Defining Internal Control Variables in Unpredictable Markets

External volatility creates market noise, yet the winning strategy isolates Process and People as the only actionable variables. Operators who control internal workflow efficiency outperform peers reacting to energy price shocks when macro indicators fracture. Rigidity regarding national averages conflicts with the flexibility needed to retain top talent in a tightening labor market.

- Audit current intake workflows for missed inspection opportunities.

- Calibrate technician compensation against local retention metrics rather than broad CPI data.

- Deploy diagnostic tools capable of handling high-voltage system anomalies.

Focusing on these internal levers transforms external chaos into a structured competitive advantage.

Implementing Intake Efficiency and Repair Order Metric Tracking

Service advisors must present thorough inspections rather than just writing up the complaint to capture revenue lost to digital competitors. Traditional retailers now compete against e-commerce sectors. Operators must transition from passive order-taking to active diagnostic presentation to survive this structural shift. Tracking specific metrics reveals hidden inefficiencies in the repair Process.

- Calculate hours per repair order daily to identify diagnostic delays before they compound.

- Monitor the proven labour rate against billed hours to detect undercharging on complex vehicle maintenance.

- Analyze the parts-to-labour ratio weekly to balance inventory turnover with technician productivity.

Indexbox data suggests this aging fleet requires more frequent interventions, yet inflation pressures limit consumer spending power. Shops that fail to optimize intake workflows miss the opportunity to convert necessary maintenance into authorized repairs. Speed of throughput conflicts with depth of inspection; rushing intake reduces the hours per repair order but sacrifices long-term customer trust. Excessive deliberation stalls bay availability. Precise metric tracking allows shops to navigate this cost by identifying exactly where time converts to value. Ignoring these internal variables leaves revenue exposed to external market volatility.

Advisor Training Checklist for Retention and Competitive Advantage

Top talent exits shops lacking clear career pathways. Operators must prioritize structured development over reactive hiring.

- Audit current mentorship programs against the specialized needs of aging fleets, noting that standard passenger parts dominate while niche automatic tire inflation systems require specific expertise.

- Implement regular diagnostic workshops to bridge the gap between theoretical knowledge and practical application on older vehicles.

- Define career pathways that reward mastery of complex diagnostics rather than just speed, countering the industry trend where deferred maintenance becomes costly repairs.

| Training Focus | Retention Impact | Operational Risk |

|---|---|---|

| Diagnostic Depth | High Loyalty | Missed Revenue |

| Career Mapping | Reduced Turnover | Talent Drain |

| Mentorship | Skill Transfer | Knowledge Silos |

Shops ignoring this human element fail to capture revenue from consumers holding vehicles longer due to affordability constraints. The competitive advantage lies in transforming advisors from order-takers into trusted consultants who explain these economic realities. Products and Brands (productsandbrands.com) offers modules specifically designed for this economic climate. Without deliberate investment in Process and People, shops surrender margin to competitors who improved articulate value to cost-conscious drivers.

About

Ray Donnelly, Master Automotive Technician and Aftermarket Parts Authority at KZMALL Auto Parts, brings over two decades of frontline experience to the complexities of the current automotive aftermarket. Having transitioned from running an independent repair shop to leading technical content strategy, Ray understands exactly how macroeconomic volatility, tariffs, and labor shifts impact daily shop operations. His unique perspective bridges the gap between high-level economic trends and the practical reality of sourcing hard parts and consumables under pressure. At KZMALL, a global B2B platform specializing in standardized ACES/PIES fitment data, Ray applies his ASE Master Certification to help navigators mitigate supply chain disruptions. By using KZMALL's extensive catalog of 50,000+ SKUs, he guides shop owners through turbulent markets, ensuring they secure reliable inventory despite global trade headwinds. His insights are grounded in the daily challenge of preventing comebacks while managing costs, making him uniquely qualified to analyze the road ahead for independent retailers facing today's economic uncertainty.

Conclusion

New vehicle sales are contracting by 4.3% in 2026. The aftermarket faces a critical inflection point where volume reliance becomes a liability. The real breakage occurs not in demand, but in the operational efficiency required to service a fleet kept on the road well beyond traditional lifecycles. Rising input costs and tightened credit conditions mean shops can no longer absorb inefficiency through sheer throughput. The margin for error vanishes when every repair order must justify itself against a backdrop of consumer financial strain.

Operators must immediately pivot from speed-focused models to diagnostic-led revenue strategies before the next fiscal quarter. This is not about waiting for market stabilization; it is about securing viability while competitors remain reactive. If your shop cannot articulate the specific value of extending a vehicle's life by two years, you will lose that customer to a provider who can.

Start by auditing your current advisor training modules this week to ensure they address complex diagnostics for aging fleets rather than simple part swaps. Replace generic sales scripts with data-driven consultations that explain exactly how preventive maintenance offsets rising fuel and financing burdens. Only by embedding this technical depth into your frontline interactions can you capture the sustained revenue hidden within the current economic stagnation.

Frequently Asked Questions

High acquisition costs force owners to keep older vehicles longer. With new vehicle prices exceeding $63,000, consumers cannot afford replacements, driving consistent demand for maintenance services on their existing aging fleets.

Surging crude prices from $70 to over $100 disrupt petrochemical feedstocks. This creates tightness in parts availability, requiring shops to plan inventory carefully to manage supply chain pressures effectively.

Affordability constraints and stalled financing prevent new purchases, aging the fleet. As monthly payments hover around $1,000, drivers extend vehicle life, directly increasing the volume of required repair work.

Economic uncertainty shifts spending from discretionary upgrades to critical safety repairs. While fuel costs may suppress driving, deferred maintenance eventually comes due as expensive, essential fixes for dependent drivers.

Operators should ignore macro panic and optimize internal operations instead. Doubling down on personnel training and process refinement yields measurable ROI better than chasing fleeting market trends during volatile periods.